If there is a single idea that defined beauty and wellness in 2025, it was this: The industry stopped pretending that everyone was playing the same game.

For years, capital markets and pundits treated beauty as a broadly rising tide, one where good branding, decent execution and enough venture or private equity backing could carry almost anyone forward. That illusion collapsed in 2025.

Last year, structural advantages compounded brutally, and structural weaknesses became fatal. The distance between the “haves” and the “have-nots” didn’t just widen; it became a chasm. Scale, balance-sheet strength, operational discipline and timing mattered again. Storytelling alone did not.

What 2025 revealed was not a temporary cycle, but a sorting mechanism. Some companies emerged with more strategic freedom, more capital and more optionality than ever. Others discovered, generally too late, that leverage cuts both ways, brands age and turnaround narratives expire faster than debt.

The Have-Nots

Estée Lauder: Stabilized, But Late to the Fight

Estée Lauder spent most of 2025 licking its wounds after a brutal three-year stretch in which nearly everything that could go wrong, did. To its credit, and under the leadership of new CEO Stephane de La Faverie, the company appears to have stabilized. It is cleaning up its portfolio and pruning underperforming assets, and—perhaps most importantly—shifting reliance from chronically ill channels like department stores, travel retail, and China, toward the U.S., Amazon, and DTC. Estee also aggressively reduced and re-balanced headcount (briefly earning the new CEO the nickname “The Terminator”) to better align the organization to its new portfolio and channel strategy.

This is a retreat to more defensible terrain. It is also about five years late.

Still, better late than never. The reset buys Estée time—time to regroup, marshal capital, and prepare for a renewed offensive posture, including M&A, in late 2026 or early 2027. In 2025, the market rewarded the stabilization effort: the stock briefly dipped below $50 (a price last seen during the Obama presidency) before recovering to close the year at $106—roughly a 40% rebound. Still a far cry from the peak of $349 reached in 2022.

A comeback, yes. A triumph, no.

Kering: Sweet Surrender

Is Kering really a beauty company? Should it even be on this list? For a brief, dazzling minute, it was.

Similar to Michael Jordan’s baseball career, Kering’s foray into beauty was short and sensational before it finally came to its senses and decided to stick to its knitting.

It wasn’t for lack of effort. Kering threw everything at beauty: money, talent, time and attention. The company spent $4 billion [gasp] buying Creed from Blackstone to serve as the cornerstone of a new beauty division. Kering hired top execs from beauty powerhouses and told anyone who would listen that the days of licensing its crown jewels to third parties were ending. Kering was not interested in just royalty checks; it wanted diversification and a better multiple. Executives at Coty, the biggest licensor of Kering brands, probably began mainlining antidepressants around this time.

Kering’s move ultimately failed. It overpaid for Creed at the peak of the market just as demand for its core luxury leather and fashion businesses slowed sharply, tanking its P&L. And it turned out that Creed, far from being an aircraft carrier from which Kering could project power, was more like a luxury yacht that needed constant and expensive maintenance. By the second quarter, Kering’s stock was trading at a 10-year low.

Faced with balance-sheet reality, Kering chose survival over aspiration and surrendered the future of its fragrance ambitions to L’Oréal, a colossal coup for Clichy. The deal was packaged as a joint venture, but everyone knows what went down. In exchange for the fashion licenses, L’Oréal agreed to take Creed off Kering’s hands and throw them a much-needed financial lifeline. The market liked the plan. Kering’s stock bounced on the news and ended the year up ~40%, handing new CEO Luca de Meo an early win.

In truth, this was an excellent deal for both sides. Had Kering not wandered off the reservation, the deal would have been seen not as a surrender, but an upgrade. As for Coty, well, read on.

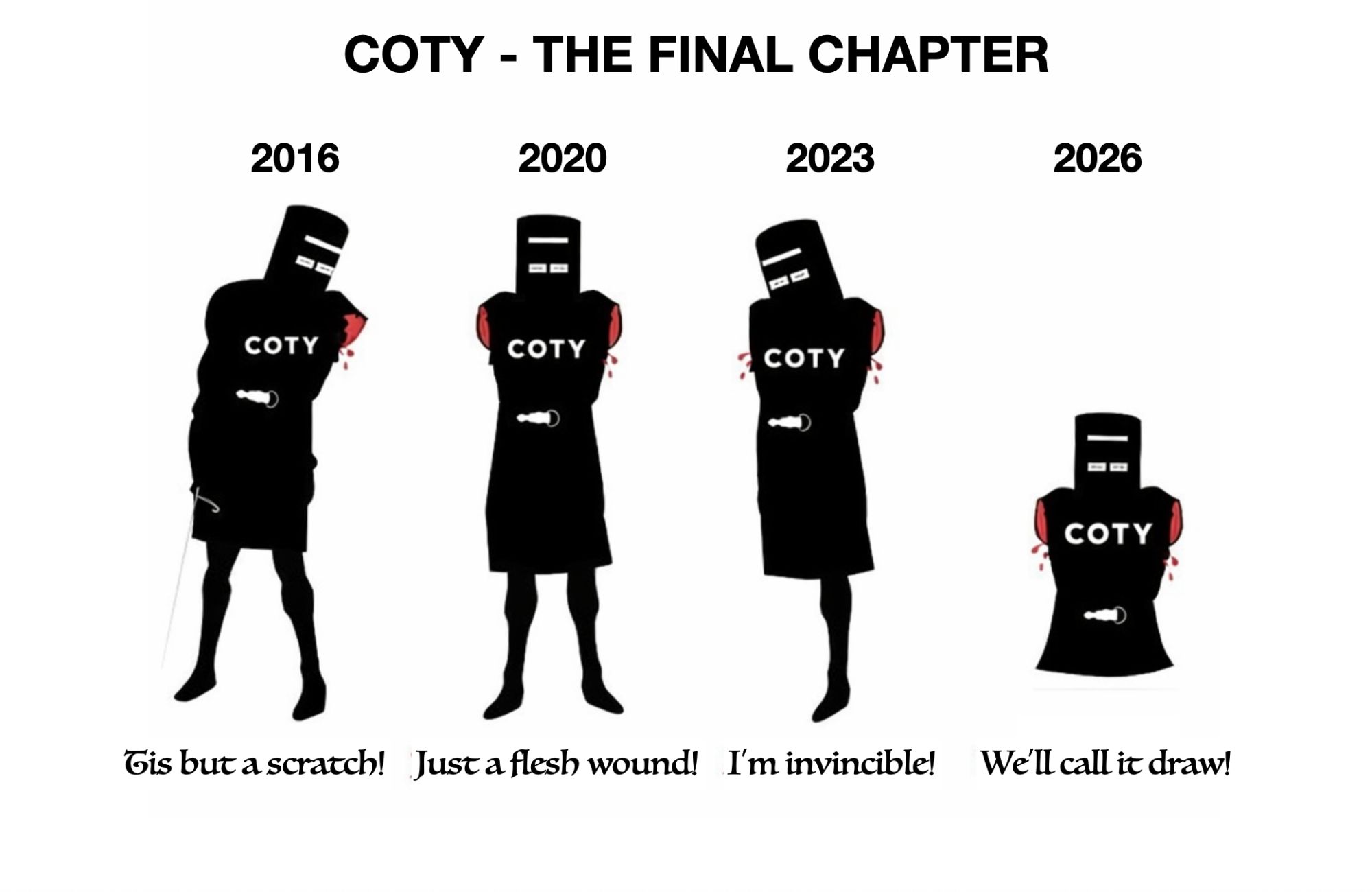

Once Mighty, Now Coty

The biggest have-not was Coty.

2025 was the start of the final chapter of what could be the single greatest value destruction saga in the history of beauty and wellness. The story began in 2016, when Coty bet the farm on a roughly $12 billion acquisition of Procter & Gamble’s beauty portfolio, the largest beauty M&A deal ever at the time. Coty, at best an upper-mid-tier operator, simply did not have the systems, processes, management depth or balance sheet to absorb and revive such a sprawling collection of aging assets.

What followed was a decade of mismanagement: a revolving door of CEOs, desperate pivots, including a $600 million Kylie Cosmetics investment, half-measures such as a KKR hair joint venture and chronic strategic whiplash. The only clear financial winner was the final CEO, Sue Nabi, who reportedly walked away with somewhere between $150 million and $300 million, thanks to a well-timed “dead cat stock bounce” during the post-pandemic fragrance boom.

Outside of that blip, Coty’s fate was sealed. Its balance sheet was too weak. Its processes were too inefficient. Its brands lacked momentum. Starved of capital, Coty could not invest its way back to relevance. The final blow came in 2025, when Kering took its long-term Gucci fragrance license away from Coty and awarded it to L’Oréal. That decision was an epic coup de grâce.

Coty’s stock sank 55% in 2025 and today it sits on the operating table, its remaining viable organs being harvested, priced and likely sold to the highest bidder.

The Haves

L’Oréal: The Heavyweight Champ

Towering above everyone is the King Kong of Clichy: L’Oréal.

It’s fashionable to mock L’Oréal for being too big, too bureaucratic, too political. But 2025 proved that whatever L’Oréal has been doing for the past decade has worked better than almost anyone predicted. Its vast portfolio is perfectly balanced across categories, channels, price points, and geographies, allowing it to absorb shocks that crippled peers like Lauder.

Unlike Shiseido, L’Oréal made the U.S. and most of its indie acquisitions work. Unlike Coty, it paired financial discipline with governance rigor to build a formidable war chest and a stable and empowered senior leadership. That war chest enabled L’Oréal to shop opportunistically in 2025, sealing Color Wow, Medik8 and transformative fragrance deals tied to Kering, executed at the time, place and price of its choosing, while most of its competitors were distracted, either reorganizing or fighting for survival.

Seeing the rise of aesthetic medicine, L’Oréal also increased its stake in Galderma from 10% to 20%, an otherwise embarrassing U-turn after selling its 50% stake in 2014. But L’Oréal, like the honey badger, does not care. Business is business.

In 2025, L’Oréal’s stock rose roughly 10%, in line with the broader CAC index, while increasing its dividend payments. Boring? Maybe. Reliable and dominant? Absolutely.

Ulta: Finding Steel

Right behind L’Oréal in the winners circle is Ulta.

2025 was the year Ulta found steel, specifically, Keisha Steelman, its new CEO. After a rough 2024 that saw the stock plunge nearly 44%, Ulta looked trapped between Amazon’s scale and Sephora’s prestige machine. Too big to grow like before. Too small to fight giants head-on.

Steelman focused on what Ulta had: a strong balance sheet and 40 million loyal customers. She exploited competitors’ weaknesses: Amazon’s lack of physical retail and growing market fatigue with Sephora. She revamped the leadership team, wound down unproductive initiatives, including the Target partnership, and made selective offensive moves, most notably the acquisition of Space NK, giving Ulta a real foothold in prestige and international markets.

Ulta still has work to do, especially with assortment strategy, store execution and staffing, but the market bought the turnaround. Ulta closed 2025 at an all-time high of $612, up roughly 50%.

E.l.f.: The Wild One

My final “Have” of 2025 is a controversial one, and its e.l.f.

Mention e.l.f. and half the industry swoons at the thought of the industry rebel, while the other half wishes there was a way to send them to prison for duping SKUs. I like e.l.f. because they are scrappy survivors. They know how close they came to extinction. That breeds paranoia—and paranoia breeds speed and out-of-the-box thinking.

One way E.l.f. outmaneuvers its larger competitors is by going further out on the risk curve. The acquisition of Rhode in 2025 was a perfect example. As one senior L’Oréal alum told me, “We’d never pay $1 billion for 10 SKUs out of a four-year-old celebrity brand.” Exactly.

That’s probably why CEO Tarang Amin did it. The opportunity was large enough to make a meaningful difference to E.l.f. Rhode’s profile was misaligned with traditional filters that strategics use, thus taking many other top bidders out of the running. His currency—cash plus public equity—was more attractive than private equity to the seller.

Will it work? Jury’s out. The stock briefly hit $150 in September before falling back to roughly half that by year-end, down ~30% overall.

But E.l.f. is still standing. And, in this industry, survival is the first victory.

What 2026 Will Decide

What does all of this mean for 2026?

First, the divide hardens. The winners of 2025 enter 2026 with optionality. They can invest, acquire, wait or strike. They can afford mistakes. They can dictate terms. The losers enter 2026 with constraints. Timing chooses them, not the other way around.

Second, M&A becomes more asymmetric. Deals will no longer be about adjacency or narrative elegance. They will be about control, price discipline and speed. Strong strategics will buy only what they want, when they want it. Everyone else will sell because they have to.

Third, capital becomes judgmental again. Investors will reward boring competence, cash generation and operational excellence. They will punish leverage, complexity, high cash burn and perpetual restructuring. Beauty will start behaving like a real industry again, not a vibes-based asset class.

And, finally, 2026 will not be kinder than 2025. For companies still “in transition,” patience will run out. For brands hoping to be rescued, the bar will rise. For executives banking on one more reset, there may not be another turn of the wheel.

2025 was the year the gap revealed itself. 2026 will likely be the year it widens.

Leave a Reply

You must be logged in to post a comment.