How Beauty Brands Scale After The DTC Boom: The New Channel Architecture

For much of the 2010s, the playbook for independent beauty brands was clear: launch direct-to-consumer, build community on social media, scale through paid digital and expand into retail selectively, if ever. That formula worked. Until it didn’t.

The Dawn of DTC

While legacy consumer packaged goods conglomerates debated the relevance of DTC or e-commerce channels for their businesses, brands like Dollar Shave Club and Glossier were rewriting the rules, achieving billion-dollar valuations by meeting consumers where they actually were: online, scrolling and increasingly skeptical of polished advertising. They wanted authentic stories.

Large CPG companies, meanwhile, were structurally ill-equipped to follow. Unit economics were difficult, products were bulky, price points were retailer-controlled and shipping costs were prohibitive. Supply chains weren’t built for DTC fulfillment, and the prospect of cannibalizing existing wholesale relationships kept many organizations frozen in place, their sales and marketing teams siloed rather than aligned. All in all, digital channels were margin-dilutive, and it didn’t make sense to disrupt scaled and profitable wholesale businesses for a relatively small prize.

This created a window of opportunity for emerging brands and a set of structural unfair advantages that, for a time, felt nearly impossible to replicate:

-

- Low customer acquisition costs: Meta was cheap and TikTok was not a thing yet.

- Direct access to consumer data for full funnel attribution.

- Influencer marketing felt authentic and scalable, with creators building loyal, trust-based audiences that brands could tap into.

- Prestige or masstige positioning, without retailer margins or chargebacks, resulted in greater gross margins.

The Big Reset

A series of events radically altered the DTC landscape.

2020: The Pandemic.

COVID fundamentally changed competitive dynamics. What had been “optional” for large CPG companies became existential. Store traffic collapsed. With the entire business at stake, silos within organizations broke: sales teams partnered with supply chain and marketing teams to quickly pivot to digital channels and recoup the business. Suddenly, conglomerates poured millions into Amazon, paid social, search and the emerging creator economy. Once a white space playground for indie brands quickly became a big power battleground.

As media costs surged, customer acquisition costs (CAC) followed and suddenly contribution margins were challenged.

2021: Apple’s iOS 14.5 update.

This update and the app tracking transparency framework that it introduced effectively killed the precision targeting and full-funnel attribution that DTC brands had relied on. Overnight, the ability to acquire customers efficiently and measure what was working collapsed.

2022 – 2023: Higher interest rates

To tame high inflation, the United States Federal Reserve sharply increased interest rates over an 18-month period from nearly zero to 5.5%. This action suddenly and drastically raised the cost of capital, which made it harder to raise funds to fuel growth at any cost.

By mid-2023, the unfair advantages that had defined the indie DTC era were gone. Valuations reset. Investors who had rewarded top-line growth began demanding sustainable margins, efficient unit economics and omnichannel proof points.

The 2026 Channel Landscape: Pros and Tradeoffs

Fast forward to today. Heavy reliance on any single channel, whether DTC, Amazon or one retail partner, is now a red flag for investors and operators alike. A brand overly dependent on Meta ads is seen as fragile. A brand that lives and dies by TikTok virality is seen as volatile.

Channel diversification has become shorthand for durability.

But that doesn’t mean every brand should be everywhere. For early-stage beauty brands in particular, expanding into multiple channels must be strategic, not reactive. Moving too fast into low-margin or operationally complex distribution can strain cash flow, dilute the brand and distract founders from the more fundamental work of product-market fit.

The key question isn’t, how many channels? It’s, where is our target customer, and which channels provide the most capital-efficient route (margin structure, cost of doing business and operational capabilities) to reach as many of those customers as quickly as possible?

Here’s a clear-eyed look at the channels emerging beauty brands are weighing in 2026:

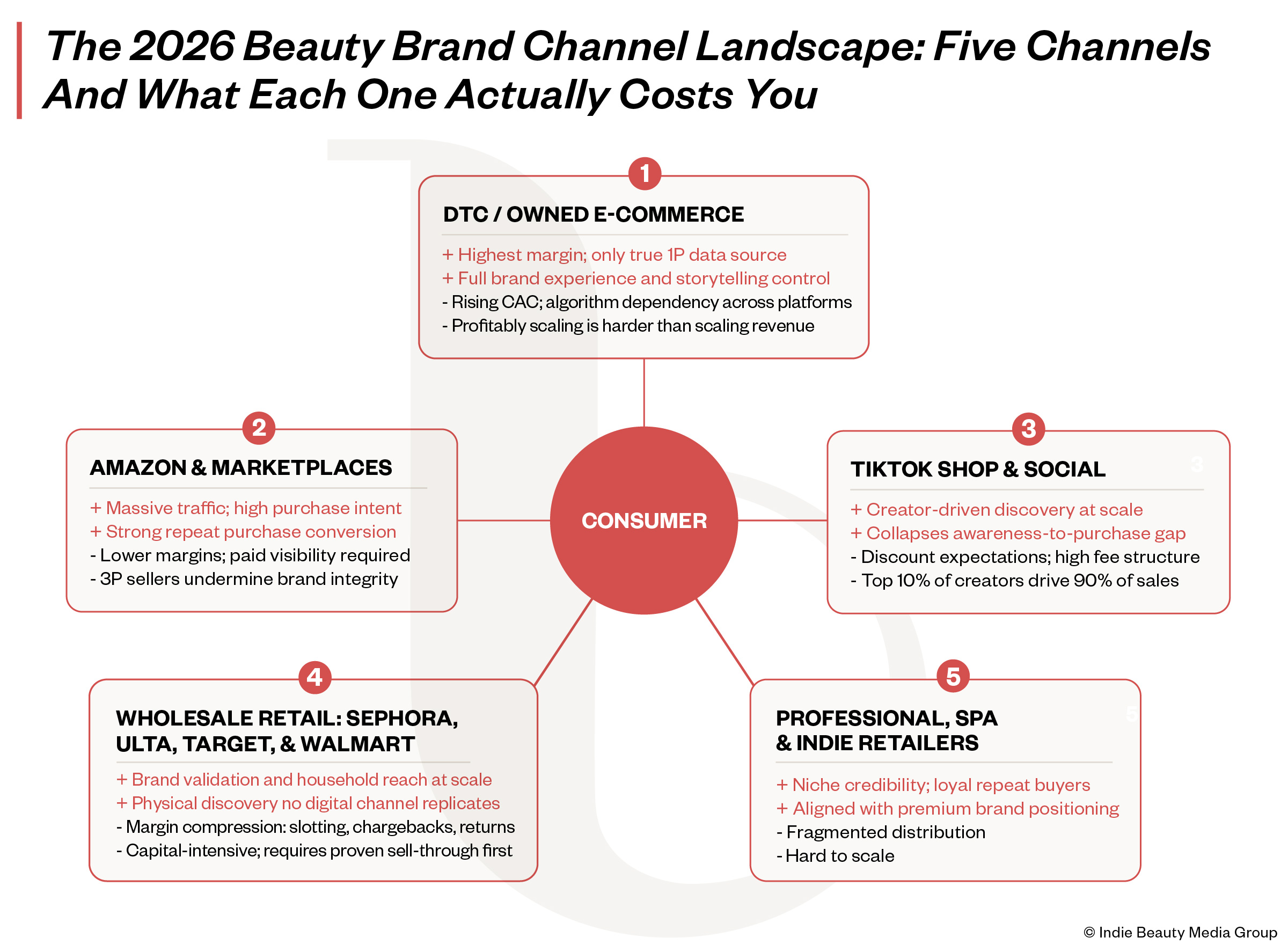

- DTC (Owned E-Commerce and Freestanding Stores): The Brand’s Home Court

DTC remains the gold standard for brand storytelling and first-party data, but it’s no longer the growth engine it once was. Profitably scaling a DTC channel today requires genuine pricing power, a strong retention strategy and disciplined creative production.

Increasingly, DTC also extends beyond the screen. A growing number of emerging beauty brands are investing in freestanding retail: brand-owned stores, pop-ups and showroom concepts that bring the online brand experience into the physical world.

When executed well, owned retail deepens community, drives discovery and creates a halo effect across digital channels. But it carries real costs: lease obligations, inventory risk, staffing and buildout capital. For most early-stage brands, brand-owned brick-and-mortar should be treated as a brand-building investment, not a margin engine, and applied with caution.

Advantages

-

- Highest margin potential provided CAC is low, but requires higher price points to enable free shipping.

- Full control over brand experience, still the only holy grail for first-party data, and the best place to learn about the customer and build community.

- Ability to test, iterate and bundle.

Considerations

-

- Rising CACs driven by media inflation and platform volatility.

- Algorithm dependency across Meta, Google and TikTok creates structural fragility.

- Requires sustained investment in content, creative and retention programs.

- Scaling profitably is harder than scaling revenue.

- Not suitable for mass price brands with bulky and expensive to ship SKUs.

- Amazon and Marketplaces: Demand Harvesting at Scale

Now the largest beauty retailer in the U.S. by volume, Amazon has evolved from a distribution afterthought into a critical proof point for brand legitimacy. It excels as a demand-harvesting channel, particularly for replenishment occasions and unbranded category searches. For brands that have built awareness elsewhere, Amazon converts it.

Advantages

-

- Massive built-in traffic with high purchase intent.

- High conversion efficiency, especially for repeat purchases.

- Operational infrastructure through FBA reduces fulfillment burden.

- Increasingly important for consumer trust and brand credibility.

Considerations

-

- Lower margins, with meaningful search and display investment required for visibility.

- Limited brand experience control, often undermined by competing third-party sellers.

- Expanding aggressively on Amazon can create friction with specialty retail partners.

- TikTok Shop and Social Commerce: The Entertainment-Driven Channel

TikTok Shop represents the newest and most volatile layer of the modern channel mix. For some indie brands, it’s been a genuine breakout growth engine capable of generating rapid awareness and conversion simultaneously. For others, it erodes margin without building lasting equity.

Advantages

-

- Content-first environment that creates brand halo across other channels, especially Amazon.

- High impulse conversion on platform; drives replenishment behavior off-platform.

- Leverages creator-driven discovery at scale.

- Reduces friction between awareness and purchase.

Considerations

-

- Requires a strong, always-on content engine to sustain performance.

- Discount-driven consumer expectations can pressure pricing and margin.

- Economics are challenging: affiliate fees, platform fees and fulfillment costs add up quickly.

- Highly concentrated: the top 10% of creators typically drive 90% of sales.

- Wholesale Retailer (Sephora, Ulta, Target, Walmart): Validation with Real Costs

Retail remains one of the most powerful proof points a beauty brand can have, but it is capital-intensive, operationally demanding and not for the faint of heart. Winning a retail partnership is the beginning of a long journey, not the destination. Founders who don’t model full landed economics before signing often find themselves in cash flow distress.

Advantages

-

- Powerful brand validation and building at scale.

- Physical discovery and built-in traffic that DTC alone can’t replicate.

- Household penetration and reach that accelerates brand awareness.

Considerations

-

- Lower gross margins than direct channels with further dilution through slotting fees, chargebacks, compliance costs and returns.

- Limited control over in-store merchandising and brand storytelling.

- Lack of data and transparency regarding consumer behavior.

- High velocity expectations require ongoing marketing investment to support sell-through.

- While brands seek to access new customers via retail, retailers themselves increasingly expect new brands to bring in new customers to their doors.

- Professional, Spa and Indie Retailers: The Overlooked Channel

Often underestimated, this channel offers something the others frequently don’t: aligned, relationship-driven distribution with genuine community credibility. For brands positioned around clean formulation, clinical efficacy or professional-grade performance, it can deliver stable, sustainable growth.

Advantages

-

- Strong community credibility within niche, high-trust audiences.

- Relationship-driven sales with potential for deep, loyal repeat business.

- Often aligned with premium brand positioning.

Disadvantages

-

- Fragmented distribution makes scaling complex.

- Resource-intensive sales management with limited infrastructure support.

- Limited reach relative to mass or specialty retail.

The 2010s rewarded focus and digital arbitrage. The early 2020s punished overreliance and capital inefficiency. Today, the market is looking for sharply differentiated brands with durable competitive advantages and a genuine moat that play in long-horizon white spaces. They want proof of dependable, sustainable growth. That means credible sales across more than one channel, but not over-distribution.

To bring this to life, consider how the same masstige skincare brand might approach its channel architecture at three distinct stages of growth:

Year 1 – 3: Early Stage ($2M to $5M Revenue, $35–$55 ASP, ~65% Gross Margin)

At this stage, the brand is DTC-only and intentionally so. A masstige price point creates enough margin headroom to absorb customer acquisition costs while building the retention flywheel.

-

- DTC is the engine. First-party data, community signal and proof-of-concept all flow from here. No retail conversation begins until the DTC foundation is solid.

- Amazon, selectively. Once awareness exists, a presence on Amazon can capture demand from shoppers already searching by skin concern or ingredient. It’s a harvesting channel, not a growth engine.

- TikTok Shop and creator content serve as awareness accelerators at this stage. Not yet a meaningful revenue channel, but critical for building brand recognition and driving traffic back to DTC.

- Wholesale retail is premature. The brand hasn’t yet built the velocity needed to support sell-through at even a boutique retailer. Ideally, a brand reaches $10 million to $15 million in profitable revenue and clear product-market fit before pursuing any retail doors.

Year 3 – 5: Growth Stage ($5M to $15M Revenue, $35–$55 ASP, ~62% Gross Margin)

DTC remains the core, but the focus shifts from proving the model to expanding reach without sacrificing margin.

-

- Indie retail is the natural next step. The Detox Market, Credo or regional independent beauty boutiques are brand-building channels as much as revenue channels. Their shoppers are highly engaged, ingredient-literate and predisposed to discover new masstige skincare.

- These partners don’t conflict with a future Sephora or Ulta conversation. They often accelerate it.

- Amazon captures replenishment from existing customers. TikTok Shop and creator content continue driving top-of-funnel awareness.

- Every channel should be earning its place. The goal: omnichannel proof points and sell-through velocity that make the brand’s next retail conversation a compelling one.

Year 5+: Scaling Stage ($25M to $40M Revenue, $35–$55 ASP, ~58% Gross Margin)

The brand has earned its anchor retail partnership. Now it’s about executing with discipline and resisting the temptation to overextend.

-

- One anchor retailer—Sephora or Ulta—becomes the centerpiece. The brand enters with proven sell-through velocity from its indie retail years, making the pitch to a major buyer far more compelling.

- DTC shifts roles. No longer the primary growth driver, it becomes the brand’s owned home court where the full story is told, loyalty is rewarded and new products are incubated.

- Amazon and TikTok Shop continue driving replenishment and discovery, particularly for new product launches.

- Resist the urge to add a second anchor retailer too quickly. Concentration in one retail partner signals white space to acquirers, a story of proven velocity, not saturated distribution. While there is no universal rule for when to open the next omnichannel retail door, caution must be applied. Move too soon and the business risks margin erosion and inventory strain. Wait too long and the window may close.

- This is the architecture that makes a brand acquirable: durable DTC economics, omnichannel proof points and a single thriving anchor retail relationship with room to grow.

While this piece has focused primarily on distribution strategy because it remains top of mind for so many founders, none of it replaces the more fundamental work of building a truly differentiated brand in a genuine white space. Before pursuing any channel expansion, founders need to be confident they have an active demand pipeline and a clear understanding of which messages resonate with their customer. Knowing what drives conversion in your own channels is what allows you to show up and perform in someone else’s.

The bottom line: there is no universally right channel mix. There are more choices than ever, which means the decisions matter more than ever. The brands that endure will be the ones that choose deliberately, execute with discipline and resist the pressure to be everywhere at once.

Oshiya Savur is a beauty industry executive with experience across prestige and mass-market segments in North America and international markets. She has worked across multiple categories, contributing to the launch of new brands, the growth of emerging companies, and the evolution of established heritage brands. Her leadership roles include positions at Maesa, Charlotte Tilbury, Revlon and Unilever in both entrepreneurial and large corporate environments. In 2024, she was named an Adweek 50 honoree.

Leave a Reply

You must be logged in to post a comment.