One Deal To Rule Over Them All

When L’Oréal announced its $4.8 billion acquisition of Kering’s beauty business last month, the consensus in beauty was simple: Alright, that’ll be it. Giant strategic deals like that are uncommon, and L’Oreal x Kering seemed like it would carry us for a while.

Then, almost out of nowhere, Kimberly-Clark strolled in with a $48 billion bid for Kenvue, casually dropping a price 10 times larger. Overnight, the L’Oréal deal, massive in any ordinary context, looked modest, and the industry found itself asking a very reasonable question: WTF just happened?

Ken-Who?

Part of the confusion stems from the fact that many in beauty don’t actually know Kenvue very well. It’s understandable. Kenvue only became its own company in 2023 after Johnson & Johnson spun off its consumer division into a standalone business. Kenvue inherited a mix of over-the-counter staples like Tylenol and Motrin, personal care brands like Band-Aid and Listerine, and beauty pillars such as Aveeno and Neutrogena.

These brands were—and still are—powerhouses, but inside J&J, a pharmaceutical giant focused on oncology, immunology and advanced therapeutics, the consumer portfolio had become the odd one out. Over years of morphing priorities, the division shrank in strategic importance, fell into a cycle of underinvestment and slowly drifted from J&J’s main mandate.

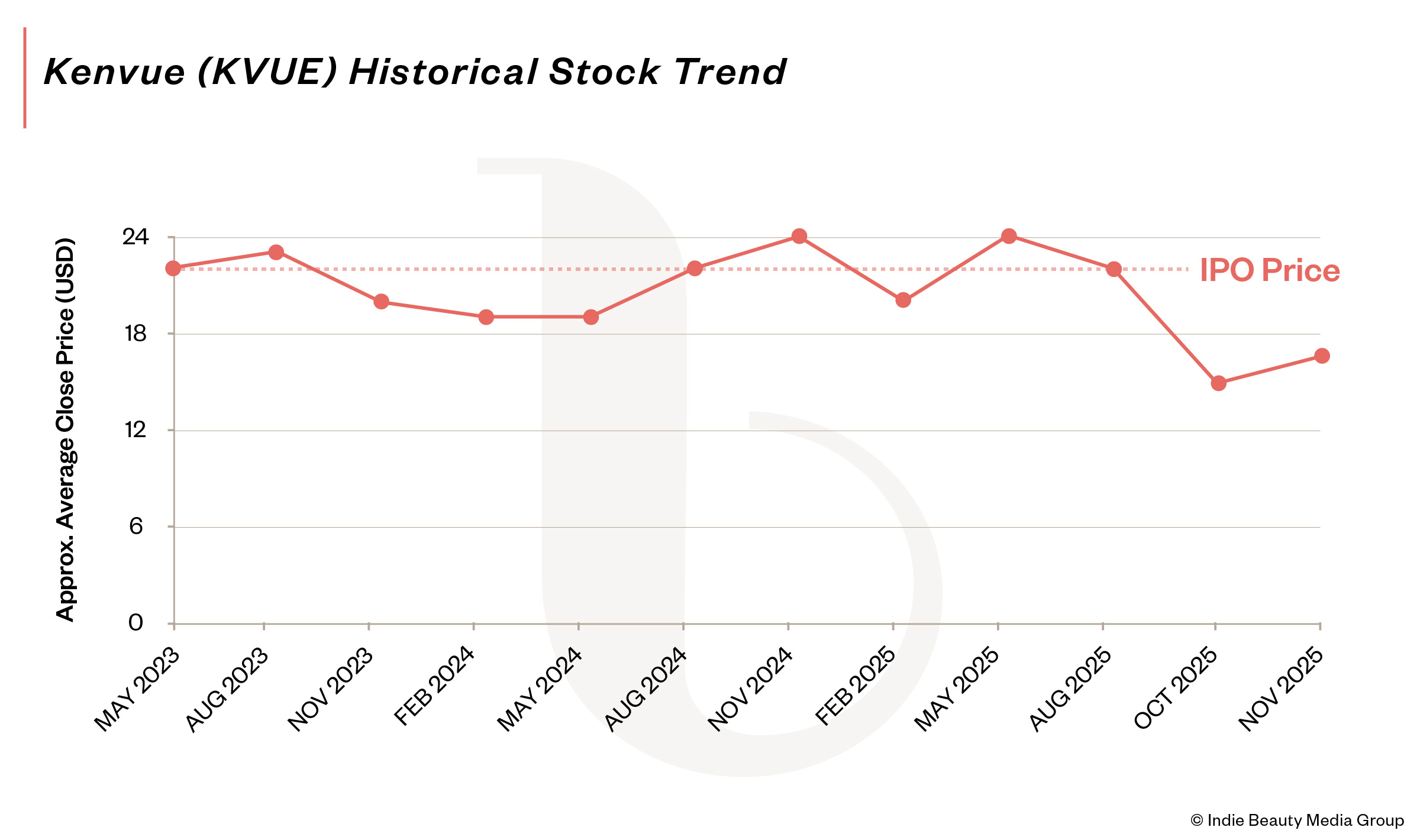

The logic of a spinoff was sound. As a standalone company with $15 billion in annual sales, Kenvue was large enough to be a major player in the categories it would need to compete. Now independent, it could reassert focus, finally invest in its business and escape the gravitational pull of a massive parent more interested in drug approvals than sunscreen innovation. The IPO price of $22 reflected real optimism that independence would unlock value. Almost immediately, though, the seas turned rough.

The Spinoff Spinning Out of Control

Kenvue’s first challenge was one few talked about openly: talent. J&J didn’t send its rising stars over to the spinoff. The team that moved into Kenvue consisted mostly of ex-J&J executives accustomed to babysitting a third-tier business behind the scenes in a massive company with deep resources and built-in support. But a newly public company is a different animal. You’re exposed. You’re scrutinized. Judgment day arrives quarterly. You need to show vision, vim and velocity.

Kenvue management was short on all of the above, and the company struggled to find its footing. Growth underwhelmed. Profitability missed expectations. The beauty business was notably soft. Soon, activist investors began circling, arguing for portfolio streamlining and suggesting that the beauty division, facing fiercer competition and a faster innovation cycle, was a poor fit for the rest of Kenvue.

Rumors intensified. A new CEO—Kirk Perry, former president and CEO of Circana—was brought in. Bankers stopped returning calls, a sign that major “strategic options” were being explored. Then came the moment no CEO, not even a newly appointed one, could’ve prepared for.

Tylenol on Truth Social

As Kenvue’s leadership was shifting, the president of the United States went on national television and effectively fired Tylenol. In an instant, one of Kenvue’s crown jewels was tarnished and became a magnet for litigation that could take decades to unwind.

The scientific basis for the Tylenol claim is as fragile and unreliable as thin single-ply toilet paper. In the middle of this surreal episode of “The Apprentice: NSAID Edition,” Kimberly-Clark arrived with a smooth and absorbent two-ply offer: it would buy the whole company in a stock-and-cash deal valuing Kenvue at around $21 per share.

Why Kim Loves Ken

On paper, the rationale isn’t absurd. From a product standpoint, Kimberly-Clark’s core revolves around categories with thin margins and slow growth: diapers and toilet paper. Kenvue plays in higher-margin categories such as skincare, haircare and oral care with globally recognized brands. From a geographic standpoint, Kenvue is present in a number of key international markets where Kimberly-Clark is either absent or weak, and vice versa.

If you’re trying to transform a slow-moving “paper products” business into a modern consumer health and beauty powerhouse with a more diversified international book of business, then Kenvue looks like an attractive shortcut. For Kenvue shareholders watching their stock drift down toward $14, the offer must have looked merciful.

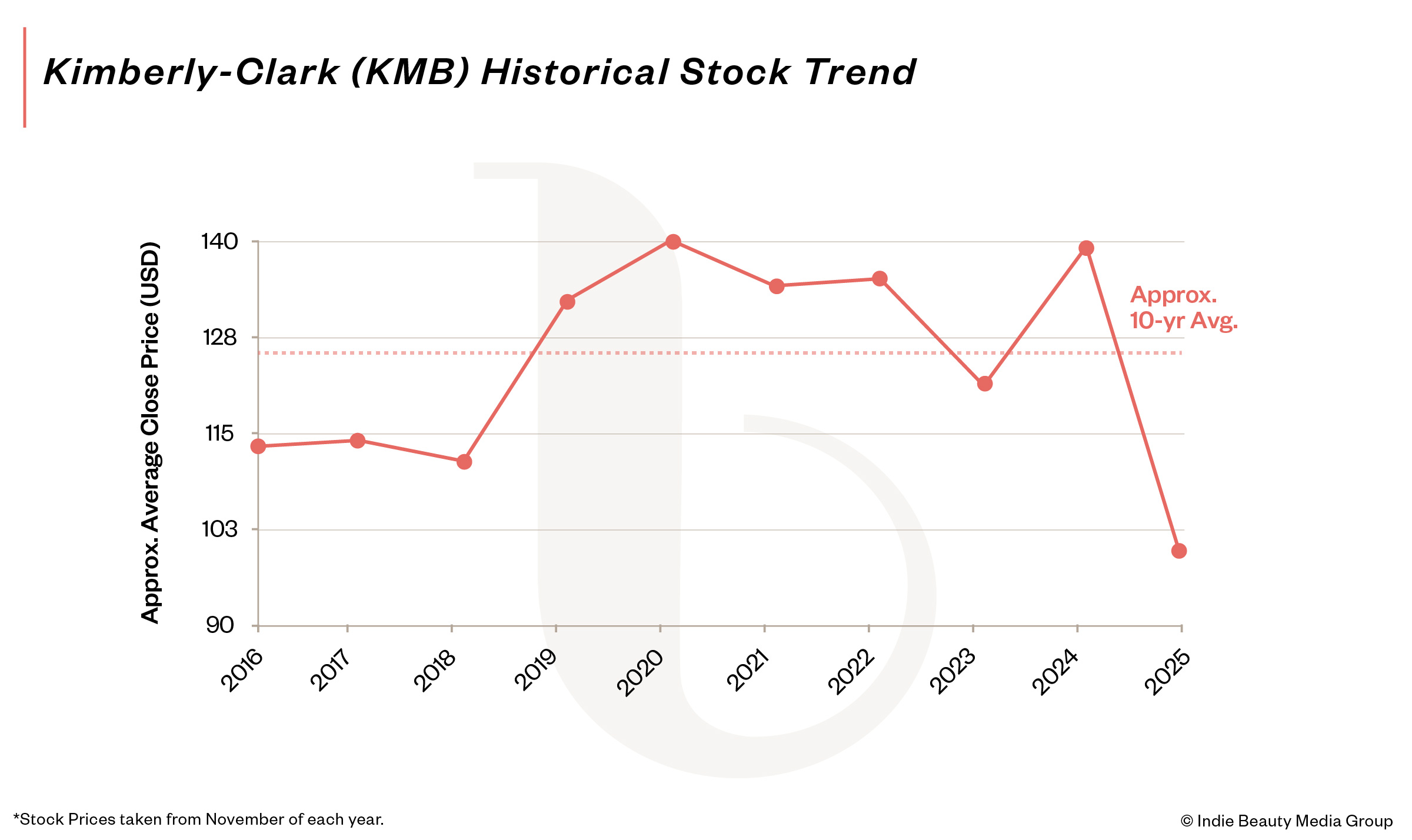

Kimberly-Clark shareholders recoiled instantly. They flushed the stock so fast that it sank to a 12-year low. They saw what Kimberly-Clark’s leadership seemed to ignore: massive, complex, high-risk mega-mergers rarely work. And when they fail, they fail catastrophically.

Mega-Mergers for the Micro-Brained

There are 48 billion reasons why Kimberly-Clark shareholders might feel abdominal discomfort. Mega-mergers have a disastrous track record. In fact, they’re considered downright unfashionable in polite financial circles. Daimler-Chrysler (cars, 1998). HP-Compaq (computers, 2001). Heinz-Kraft (CPG, 2015). AT&T-Time Warner (media, 2016). Different sectors, different periods, the same lousy outcome.

In beauty, the last deal remotely comparable was Coty’s $12 billion acquisition of P&G’s aging beauty portfolio in 2016, a transaction now canonized as a “don’t ever do this” lesson alongside blow-drying your hair in the bathtub.

Why do mega-mergers fail? Combining massive complex global businesses is mind-bendingly hard, time-consuming and expensive. Risks don’t add, they multiply. While two companies are distracted gazing inwardly during post-merger integration hell, decision paralysis takes hold, competitors move in and the best talent inevitably heads for the exit.

Those glorious “synergies”? They exist solely on spreadsheets prepared by M&A advisors paid to do the deal and rarely materialize in the real world. Other charges and impairments are almost guaranteed to appear, further distracting executives and souring the mood.

There is a more fundamental question, however. Why place Kenvue, an already rocky business, inside another conglomerate that lacks the expertise to run it? Wasn’t avoiding that the rationale for the original spinoff from J&J?

A Poor Fit

If Kenvue had to be acquired by a bigger conglomerate, there are obvious natural homes: Procter & Gamble, Colgate-Palmolive or Church & Dwight. Those companies understand OTC, personal care and beauty. They know how to manage regulatory risk and compete effectively. They can upgrade Kenvue.

Kimberly-Clark doesn’t. Its greatness lies in converting millions of trees each year into stuff you can wipe your butt with. That excellence doesn’t automatically translate into helping Rogaine fight Hims or saving Tylenol from Trumpism.

Speaking of Tylenol, even if Kimberly-Clark believed it could manage the operational complexity, it now inherits a dire threat: litigation and reputational damage that can span generations. After the president’s remarks, Tylenol became a cultural meme, one that will almost certainly outlast scientific reality. The business peril can’t be reliably sized, modeled or hedged.

If Kimberly-Clark is confident it’s fully characterized and quantified the risk with the phalanx of experts it’s undoubtedly retained, it’s deluding itself. The state of Texas, where Kimberly-Clark is headquartered, is suing Kenvue for hiding the alleged link between Tylenol and autism. Does Kimberly-Clark read the local paper?

Some have attempted to reframe the acquisition as opportunistic. They argue Kimberly-Clark is picking up Kenvue on the cheap. Conspiracy theorists suggest that Trump and Texas purposefully trashed Tylenol to help Kimberly-Clark break the will of an already dispirited Kenvue shareholder base and make its takeover bid seem appealing.

But in M&A, especially at this size, “cheap” is an illusion. There are no bargains at $48 billion. The smart bet is that this deal, like 90% of mega-mergers like it, will end up far worse for the parties involved than anyone could’ve imagined.

Ken Can Do Better

Here’s the real tragedy: Kenvue has a compelling beauty portfolio. Neutrogena’s recent sunscreen campaign with John Cena shows what happens when you bring in experienced leadership allowed to apply creativity and focus to invest and innovate. Kenvue’s beauty portfolio is far from dead, it just needs TLC.

There are many private equity firms armed with billions that would gladly buy these brands and nurture them properly. They see the potential. Beauty thrives when brands are treated as cultural assets, not as “problem children” inside conglomerates focused on diapers and tissues.

I’ll just say it, Kimberly-Clark’s strategy appears lazy, unimaginative and desperate. Rather than a thoughtful and deliberate move by a company operating from a position of strength that knows what they’re doing, it reads as a dicey shortcut taken by a desperate CEO purposefully ignoring blazing red flags, a giant risky move meant to “fix” everything by people bankrupt of better ideas.

Giant risky moves rarely fix anything. More often, they break the things that still work. Just ask Coty.

Speaking as someone in the beauty world, I hope the story doesn’t end with Neutrogena, Aveeno, Clean & Clear and OGX becoming footnotes inside a conglomerate distracted by a million post-merger headaches and a bottomless pool of product liability danger.

The brands deserve a home where they’re not only valued, but supported and understood. Their future isn’t about tissues, pulp or diapers, it’s about science, culture, storytelling and consumer connection—and those things require a different kind of steward.