Beauty spending growth is expected to be muted for the first quarter this year in the United States, according to two new forecasts.

Data provider Daash Intelligence projects beauty industry growth will be flat for the quarter, while consumer insights firm Prosper Insights & Analytics estimates that spending will increase between 2% and 2.5% from the same period a year ago. The forecasts roughly align with last year’s performance numbers for the first quarter, when prestige beauty sales were flat and mass beauty grew by 3%, according to market research firm Circana. For the first nine months of 2025, Circana data shows prestige beauty sales up 4% and mass beauty up 5%.

Daash and Prosper’s forecasts underlie beauty dynamics in which consumers are balancing a desire for affordable luxuries and everyday essentials with caution in an economic environment where confidence has fallen to its lowest level in over 10 years. Stressed by slower job growth, persistent inflation and rising credit delinquencies, consumer sentiment as measured by The Conference Board’s Consumer Confidence Index dropped to the lowest level it’s been since May 2016, even lower than the depressed confidence of the pandemic, due to present concerns and a souring attitude toward the future. Prosper Insights data reveals 41.4% of adults reporting they’re confident about the economy, down from 44.7% a year ago.

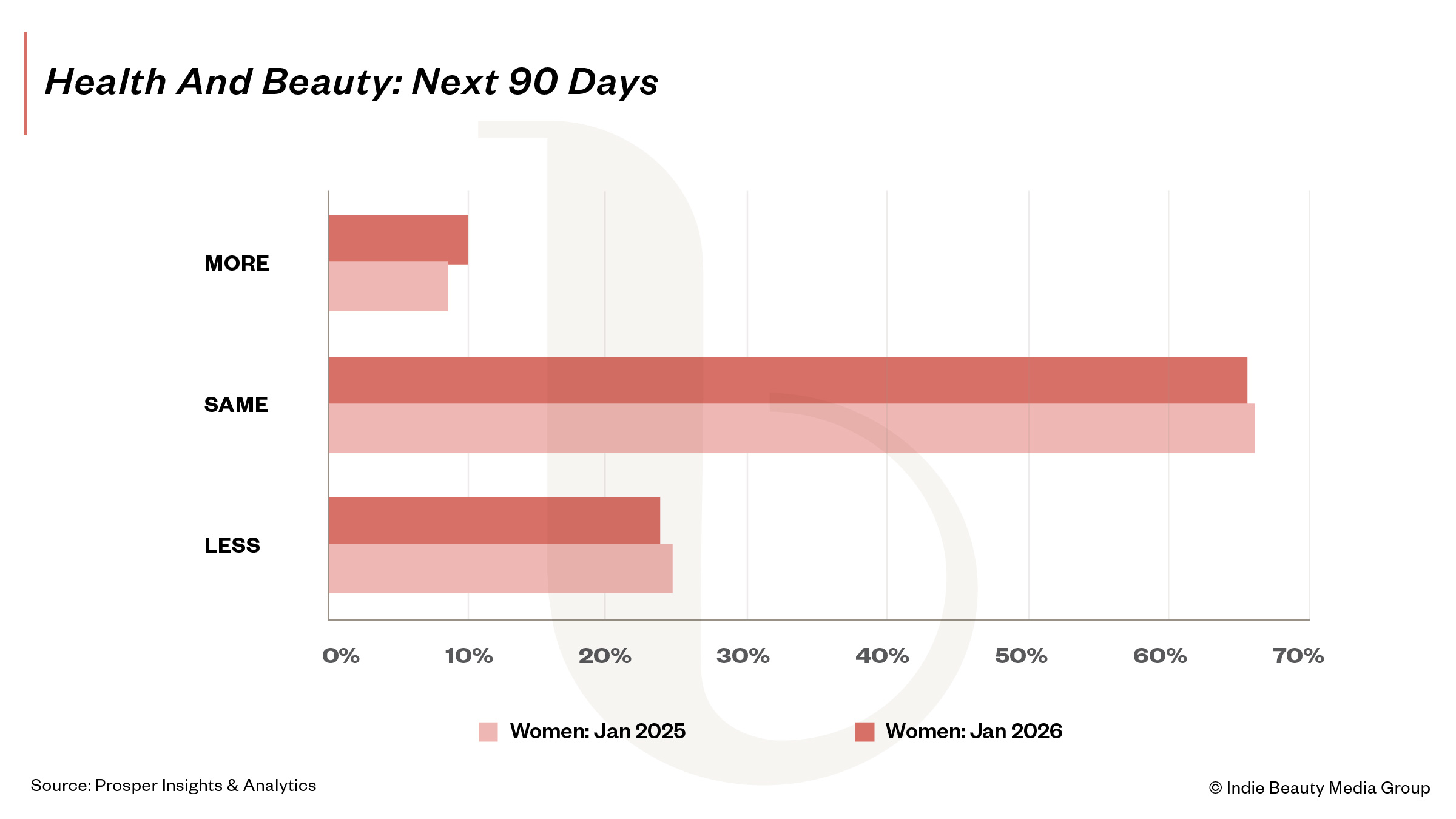

However, Americans aren’t dramatically pulling back on beauty spending. In a survey of 8,000 American adults, half of them women, Prosper Insights found that about 10% of women plan to spend more on health and beauty products in the first quarter of 2026, compared with 8.9% last year. About 23.8% of respondents intend to spend less on the category, a decrease from 24.7% in 2025, with 66.1% planning to spend the same on the category. In the same survey last year, 66.4% of women intended to spend the same amount on health and beauty products.

Melissa Munnerlyn, co-founder and CMO of Daash Intelligence, says, “Consumers are still investing, but they’re making sharper choices. The bottom line is with the state of the world people are just looking to feel good in any kind of capacity. Sometimes that means spending money on a luxury fragrance. Sometimes that means stocking up on three different shades of Summer Fridays lip balms.”

Aligning with consumer spending trends overall, consumer intelligence resource NielsenIQ data illustrates disparities in spending between higher- and lower-income beauty consumers. Anna Mayo, VP of the beauty vertical, says households earning more than $100,000 a year account for nearly half of beauty spending and are growing 18% to 20% year over year. Lower-income consumers making under $50,000 represent about a quarter of sales and are flat to slightly declining in their spending.

That split is influencing retail choices, too. A survey by global consultancy Alvarez & Marsal conducted last fall of 2,000 U.S. shoppers found that higher-income shoppers are more likely to trade down by switching to cheaper retailers rather than cheaper brands, while consumers making less than $100,000 a year are more likely to buy fewer beauty items.

“Higher-income consumers will continue spending but optimize and engage in high-low behavior, while lower-income consumers pull back selectively,” says Manola Soler, managing director at Alvarez & Marsal. “It will reinforce a polarized market and put pressure on the middle.”

Soler remains “cautiously bullish” on beauty industry growth this year. She cites Alvarez & Marsal’s survey showing a slight uptick in beauty spending intent. In contrast, she points out that grocery and personal care notched decreases in spending intent. “Beauty remains resilient relative to other discretionary categories, but growth will be selective,” says Soler. “It will be driven by perceived value and routine protection and not by impulse or blind loyalty.”

As they navigate economic turbulence, beauty consumers are trading up or down based on where they judge there to be bang for their buck. Last year, Daash data highlighted consumers trading up in haircare and down across fragrance, makeup and skincare as prestige beauty prices rose 14%. Factoring in both mass and prestige, NIQ’s most recent data indicates a price increase of 3%. Daash pegs fragrance as registering the steepest trade-down behavior, with nearly 40% of prestige fragrance growth coming from scents priced under $50.

Munnerlyn predicts that beauty shoppers will behave similarly across categories in 2026. “Categories tied to routine and real performance—hair being the standout—will continue to earn trade-up dollars,” she says. “It’s less about ‘less spending.’ People are willing to pay more where they see results…and they’re happy to be price-savvy everywhere else.”

Jonathan Cohen, CMO of skincare device brand Pure Daily Care and oral care brand AquaSonic, agrees that consumers will prioritize efficacy in their beauty purchases even as they reshuffle spend in other categories. He argues the pattern is especially true in skincare where dupes and K-Beauty have flooded the market with affordable options. Cohen says, “It becomes less about premium versus mass and more about what’s truly differentiated versus what’s replaceable.”

Munnerlyn identifies multitasking products and targeted treatments in skincare; lightweight, maintenance-focused products in haircare; affordable fragrance sprays; and lip balm mania as growth contributors. “I keep waiting for the lip balm bubble to pop,” she says. “Because it’s such a lower-price, feel-good type of product, and we haven’t changed a lot economically on the broad scale, people are still leaning in that direction.”

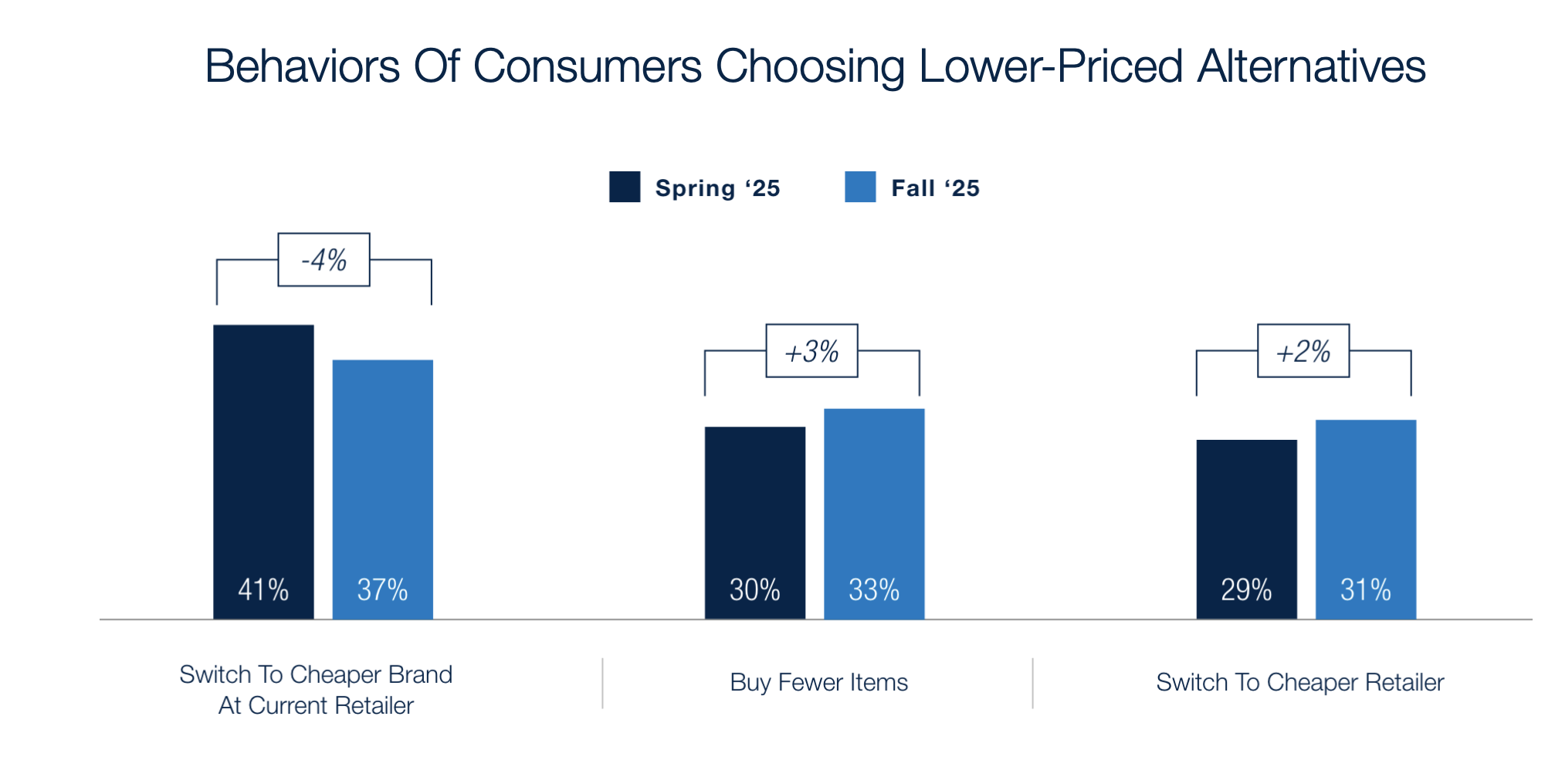

Beauty consumers aren’t just trading down in certain categories. They’re changing where they shop. According to Alvarez & Marsal’s survey, consumers’ plans to switch to cheaper retailers went from 29% to 31% between 2024 and 2025. Those that plan to buy fewer products increased 3% from 30% to 33%. Fewer shoppers reported they plan to switch to cheaper beauty brands, from 41% in 2024 to 37% last year.

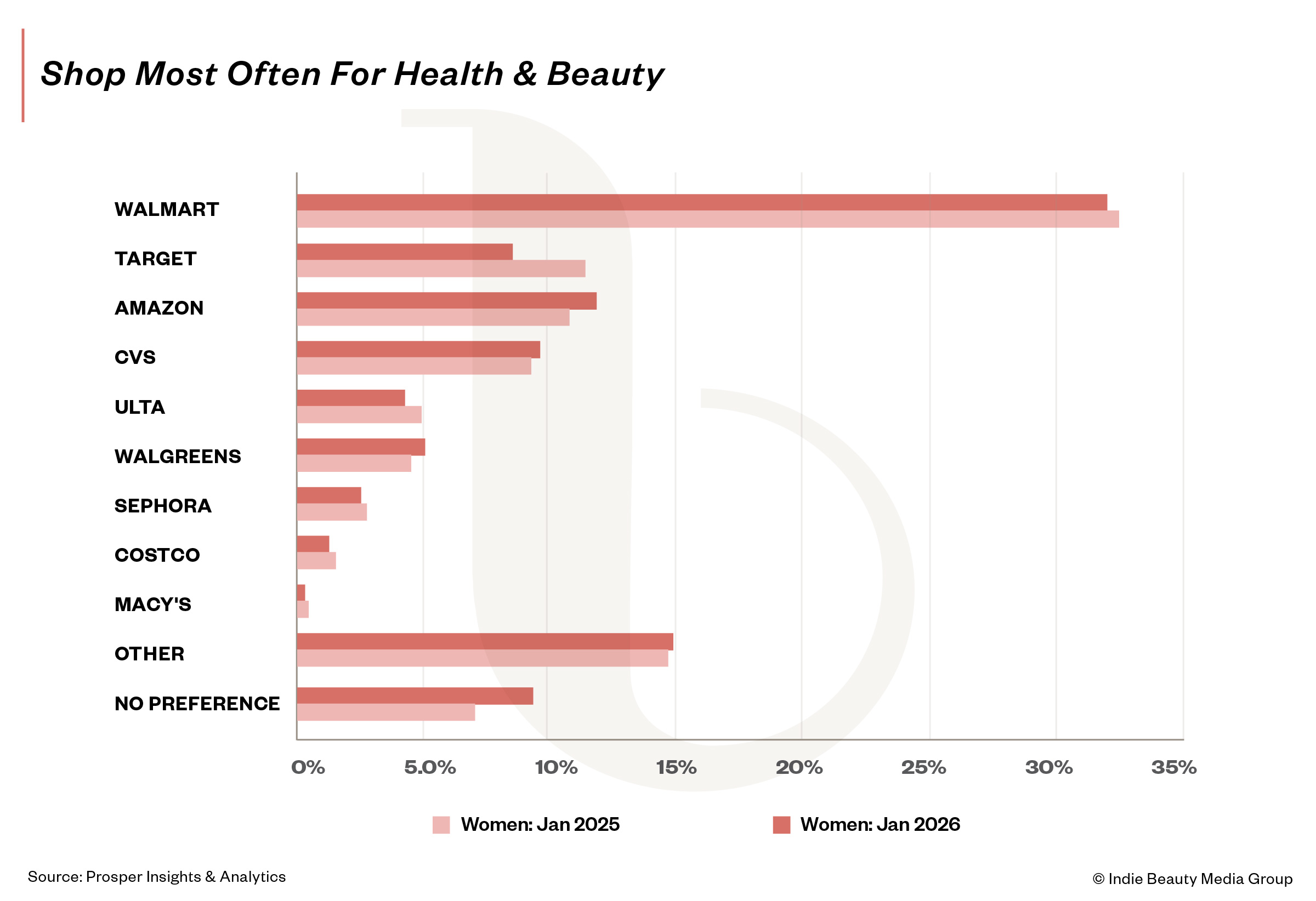

Additional data from Prosper Insights’ survey shows value-oriented retailers taking the lead with beauty shoppers. Amazon gained the most ground year over year, with 11.9% of participants saying they intend to shop most often there for health and beauty over the next 90 days. In the same period last year, that percentage was at 10.8%. The majority of female shoppers (31.9%) answered Walmart when asked where they will shop most often for health and beauty, a slight dip from last year’s 32.4%. Prosper Insights asks shoppers to write their preferred retailers when asking where they intend to shop.

Target’s draw with beauty shoppers diminished the most over the past year, with 8.6% saying they will shop there most often compared to 11.4% the year before. Sephora and Ulta Beauty remained fairly flat year-over-year. Macy’s declined in share. The category listed as “other” in Prosper Insights’ survey encompasses mom-and-pop retailers, local drugstores, grocers and salons as well as larger retailers like Neiman Marcus.

Ultimately, Cohen stresses the question isn’t whether beauty consumers will keep spending, but whether brands can keep up with where and how they now choose to discover, evaluate and buy. “The winners will be the brands that adapt fastest. Spend is shifting toward the channels where discovery and conversion are happening in real time, and toward messaging that’s clearer, more proof-driven and more value-aware,” he says. “So, it’s less ‘will people spend’ and more ‘will brands meet consumers where they’ve moved.’”

Leave a Reply

You must be logged in to post a comment.