Greycroft’s Brian Bustamante-Nicholson On His Mass Market Focus, The Agentic Web And Brand Durability

Greycroft, the 19-year-old early-stage venture capital firm crossing consumer and technology, has been bolstering its consumer bench.

After Katherine Power, who’s had founding roles in Versed, Merit, Avaline and Who What Wear, became a partner in 2023, Brian Bustamante-Nicholson, former managing director at Sonoma Brands, where he led investments in Power’s brands Merit and Avaline, came on board a year later as a partner as well. Now, Eric Ryan, founder of Cereal and co-founder of Welly Health, Olly and Method, has joined Greycroft’s consumer brand team as an advisor.

Greycroft’s consumer brand portfolio includes Mother Science, Experiment Beauty, Arey, Sisu and Seed Health, which Reuters reported last year was exploring a $1 billion sale. In partnership with L’Oréal’s VC firm BOLD, it invested in Rembrand, an AI-powered product placement platform, and the makeup brand Ami Cole. All told, Greycroft has raised over $3 billion in capital and backed more than 400 brands. This year, Bustamante-Nicholson expects it to make five consumer brand investments.

He was drawn to the firm to execute Power’s consumer brand investment thesis marrying digital and operational prowess. “Greycroft being a venture firm with one foot in technology investing is a big advantage to an investor like me on the consumer side,” says Bustamante-Nicholson. “What we’re able to do in terms of surfacing interesting technologies and companies within areas like AI that are helping brands in areas like marketing and logistics and payments is very unique. I can’t think of another firm that has that kind of capability.”

Beauty Independent spoke with him about the database of consultants Greycroft is assembling, the implications of the Agentic Web for brands, why he’s eyeing the mass market more for potential investments and two overriding trends that inform his perspective.

What brand stages do you focus on?

The fund is focused on early stage. We are evolving our strategy into investing in growth-stage brands. That’s where I spent the majority of my career. I’ve invested across everything from seed to very mature growth equity investments, but the opportunity I saw in the market that I’ve executed upon for the past seven years is identifying brands that have some quantifiable level of product-market fit. You’re catching them at exciting inflection points where they might have a great direct-to-consumer business with an Amazon business and the opportunity to get into retail in a big way.

What that typically means are businesses between $3 million and $20 million in revenue growing very fast, where they’re a click below the size that the more established consumer private equity firms are investing, and where we feel like we can generate the best risk-adjusted returns. What I’ve learned in my career is you can solve for that product-market fit equation earlier and earlier as time goes on because of what’s happened largely with technology and the amount of channels now that brands can succeed in.

How do you validate product-market fit?

It’s two things. It’s channel metrics and the financials. On the channel metrics, it’s retail unit velocities, sell-through, the amount of doors. It’s being able to look at the early signs to draw conclusions.

Then, what we’re finding more are businesses that have strong direct-to-consumer metrics—obviously, repeat purchase rate, retention, lifetime value to customer acquisition costs, if there’s a subscription component to it. I always look for low ratio of paid marketing to revenue, typically that means spending below 20% of your total sales.

Financial performance, meaning high gross margin structure, unit economics and a path to profitability. That’s a powerful equation if you can tie all that together, sound financials and compelling channel metrics.

We’re finding businesses that can show some of those direct-to-consumer metrics early on, maybe show success on a third-party marketplace like Amazon or even TikTok Shop. That’s a different world than say 10 years ago, obviously when the path to success was you had to keep knocking on the door of Sephora or Ulta to get placement there and then that would get more success potentially. They were king makers.

You mentioned inflection points. Does a brand have to have a purchase order from Sephora or Ulta for you to get involved?

They’re not prerequisites. Part of our value proposition is being able to identify brands that have the opportunity to show well in front of those retailers, but, secondly, to help them along in their journey to be successful in those retailers.

What is important is us seeing a path into retail because I think the days of investing in purely direct brands are over. I don’t think strategics particularly want a direct-to-consumer business. Rhode is an outlier. Dollar Shave Club and a few others have not turned out to be very successful acquisitions.

Within beauty and wellness, what spaces are you especially looking at now?

We’re very excited about fragrance. We think there’s a big opportunity there both at the prestige and mass levels. That’s on the radar of everybody. It’s still underdeveloped as in there’s still a lot of opportunity there. We see a bunch of new brands focus largely at the prestige level, but it’s early days, and we’re not seeing a lot of folks going after the mass part of the market, which we think is the most attractive part of the market.

Why is mass the most attractive part of the market to you?

There’s the most opportunity to build big brands for consumers there. Most of the innovation that happens with new entrepreneurs they’re building at the prestige level. They’re not paying a lot of attention to the mass shopper.

In personal care and body, when you talk to strategics, there’s a lot of interest in those areas. That area could benefit from the things we’ve seen in terms of infusing wellness and functional ingredients into formulations. We’ve seen a lot in more skincare, haircare, but less into areas like body.

We saw venture capital enter the consumer space and then depart. With a spate of deals in the consumer space, from Poppi to Rhode, there’s talk of the investors returning to consumer. What’s your thoughts on that?

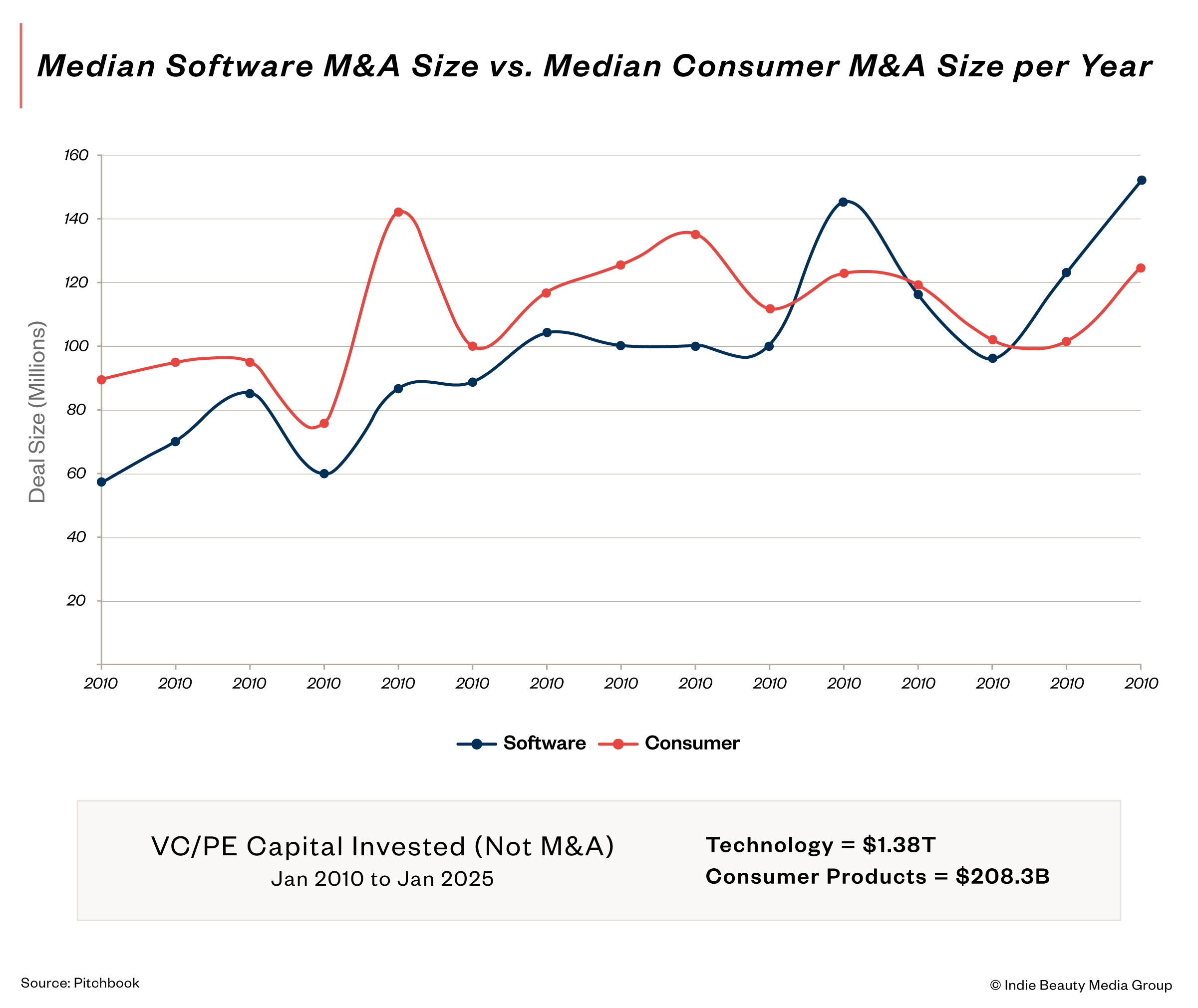

My thoughts are consumer never really left. We crushed the data here. If you look at the number of M&A deals and the median value going back the past 10 years, tech is maybe 3% higher in terms of the median deal value, but it’s roughly the same in terms of the number of actual deals.

How much capital has been invested into tech over those 10 years? Over a trillion. That’s eight times more than what was invested in consumer with roughly the same number of outcomes. That tells you that consumer has been more capital efficient. It doesn’t have the dynamics that you see in tech that garners all the headlines in terms of the public companies happening.

Silicon Valley investors came in and two things happened. The first is they didn’t know how to value these businesses, so they were throwing together term sheets and valuations that value them like software businesses that were looking at revenue multiples. That screwed up the market.

Secondly, they were investing into businesses that were growing fast without understanding the roadmap. They didn’t understand the strategic priorities of the Estées, Shiseidos, P&Gs and Unilevers. When you don’t understand that, you might end up with a fast-growing electric toothbrush brand, but nobody needs to own that business.

When nobody needs to own that business on the strategic side, who are your buyers? They’re probably private equity firms. It’s going to take you a long time or maybe never to get out of these businesses to a financial sponsor that’s going to value the business based on an EBITDA multiple and not anywhere near the price you paid as an investor coming in.

And what we’re seeing right now is the tourists have left, and now we’re dealing with the M&A markets becoming much more rational. If you look at the large outcomes in the space, everything from Rhode to Touchland to Hero, these things were valued on EBITDA multiples. They weren’t valued at eight times revenue. They were valued in the teens of EBITDA multiples, which is where the industry has historically been.

When you look at the recent big deals, what piqued your interest in those deals that the average layman might not notice?

It comes down to the strategic value that these businesses are serving, but what’s also important is compelling financial profile of these businesses. A lot of entrepreneurs in this space think, well, If I build a fast-growing haircare line that’s prestige focused and selling well at Ulta and Sephora, I can exit this business at some kind of multiple of revenue, and it’ll be great. I think strategics are much more focused on the financial profile being as prominent a factor in their decision as the new cool, innovative brand.

If you could reverse engineer the brand that you’re talking about that’s better suited to an exit today, what would it do?

It is making sure that the business profile has the right foundation to drive meaningful EBITDA margin, think 15%-plus EBITDA margin. You have to put yourself in the seat of the strategic. They want to buy something that they feel can compound over the next 10, 15 years and will be a great provider of earnings for them. If you are too focused on the sizzle of revenue growth and channel expansion, you’re probably not going to be very happy with the result.

In a LA Business Journal interview with you, you mentioned looking for businesses growing at a 300%-plus rate.

We want to see a business going from $500,000 to $3 million, that kind of early growth traction. But, at the end of the day, it comes down to what I said in terms of that product-market fit. We’re trying to find businesses that have these outlier metrics, whether it be from a pure digital standpoint or a retail standpoint.

Growth is important, but even more important is finding things that are, for lack of a better word, anomalies. And you can start to find those things earlier and earlier because of the number of channels that these businesses are able to start on.

There’s a lot of discussion about the collapsing distance between beauty and wellness. What do you make of that?

The big trend within beauty has been better-for-you and people realizing what they’re putting on their bodies is as important as what they’re putting into their bodies. It’s created the opportunity for beauty brands to behave like wellness brands in terms of bringing in functional aspects to the formulations. That’s only going to continue.

Conversely, wellness brands and even food and beverage brands are behaving like beauty brands. Eric Ryan likes to say that all the trends within CPG around brand and messaging start on the beauty side.

There are two undeniable huge trends that are going to be driving consumer for the next 20 years. It’s the digitalization of everything, and it’s better-for-you.

If you had to boil down how you assess brands, what’s the biggest thing you’re looking for?

The ability of a brand to be enduring. I know that sounds esoteric, but we are really trying to find businesses that are going to be here for the next 20, 30 years and are going to be durable compounding businesses. If you look at something through that lens, then what you’re really focused on is the quality of the product, the points of differentiation, the quality of the management team and the addressable market for these businesses.

There’s a lot of entrepreneurs building for the 1% of the 1%. We believe there’s a great opportunity to deliver premium aspirational-type products at price points that are accessible and create much, much bigger addressable markets.

Your portfolio today doesn’t necessarily reflect a focus on mass.

We aren’t dogmatic. We are opportunistic. I personally think that there’s a big opportunity within mass. It doesn’t mean that two weeks from now you won’t hear about us investing in a more luxurious-type product.

On the prestige side, we have to believe that the business can be more compelling in terms of the ability to get to profitability. The challenge that you have to focus on is, how big can this business really be?

On the mass side, you’re dealing with the converse problem of trying to create a price point that’s accessible and you’re doing it to the detriment of the margin profile of the business. In some cases, it’s more difficult than underwriting a prestige product. If you invest into one of these businesses where it ends up being largely a club type business—Costco and things like that—you better be sure that you’ve got the right margin profile.

How has building a team for early-stage businesses changed?

We see more companies doing more with less people. It is profound. Six or seven years ago, I never saw businesses that were able to generate multimillion-dollars of revenue with six FTEs. You’re seeing that now.

You’re seeing entrepreneurs leveraging more fractional employees. I see founders that are hiring more advisors as consultants to even leading marketing for them and interact with them a couple times a week on a phone call and then hiring a junior person to execute against what’s been driven by those consultants. On top of that, you’re starting to see brands doing more with less because of AI tools, particularly around marketing, creative content.

I’m creating a proprietary network and database of talented operators. The purpose of that database isn’t just to put full-time employees into more portfolio companies. It’s really to be able to leverage high-level senior executive functional experts that we can bring in as consultants and board members to our companies. We believe that that’s where the world is going, where you’re able to get a little piece of somebody here and there.

How do you advise smaller brands to create successful boards?

Doing it sooner rather than later is a good idea. It creates accountability for the entrepreneur, but also for the board members. We encourage our founders to use us in terms of being board members as extensions of their management team.

A good founder won’t just report what’s going on in the business every quarter. The real focus of the board meeting should be on, these are the key decisions that we are grappling with, and I need you to help as a board member. A good founder will want that level of expertise on the board.

What significant development are you watching closely?

The Agentic Web. How we interact with websites and with brands is going to change. It is going to be more agent-driven. We’re going to enter a phase where consumers are directing agents to do things, and they’ll be not just tools of research and finding answers, but they’ll actually be proactive in doing things for us.

It will create a way for brands to almost like SEO to build digital experiences that will enable them to be found to interact with agents and help facilitate transactions. I think it’s going to be here in a couple of years.

What should brands be doing to prepare?

They should be creating a lot of content because content is their way to be found. If you put yourself in the perspective of directing an agent to go find you something, they’re probably going to look for brands that have a high degree of content that feels authentic and trustworthy, things like reviews.

Brands really trying to enhance their digital footprint right now is a good idea. A core part of our lens is looking for brands that have real expertise around digital, content creation, community building and an innate understanding of building towards where the world is going. Even if it’s a retail-driven business, you have to have what we call digital DNA.

This article was updated on July 9 to clarify that Eric Ryan is an advisor at Greycroft.