Indie beauty brands continue to siphon market share from conglomerates as emerging players stoke curiosity, drive shopping trips and hold back on price increases that their larger rivals are pushing through.

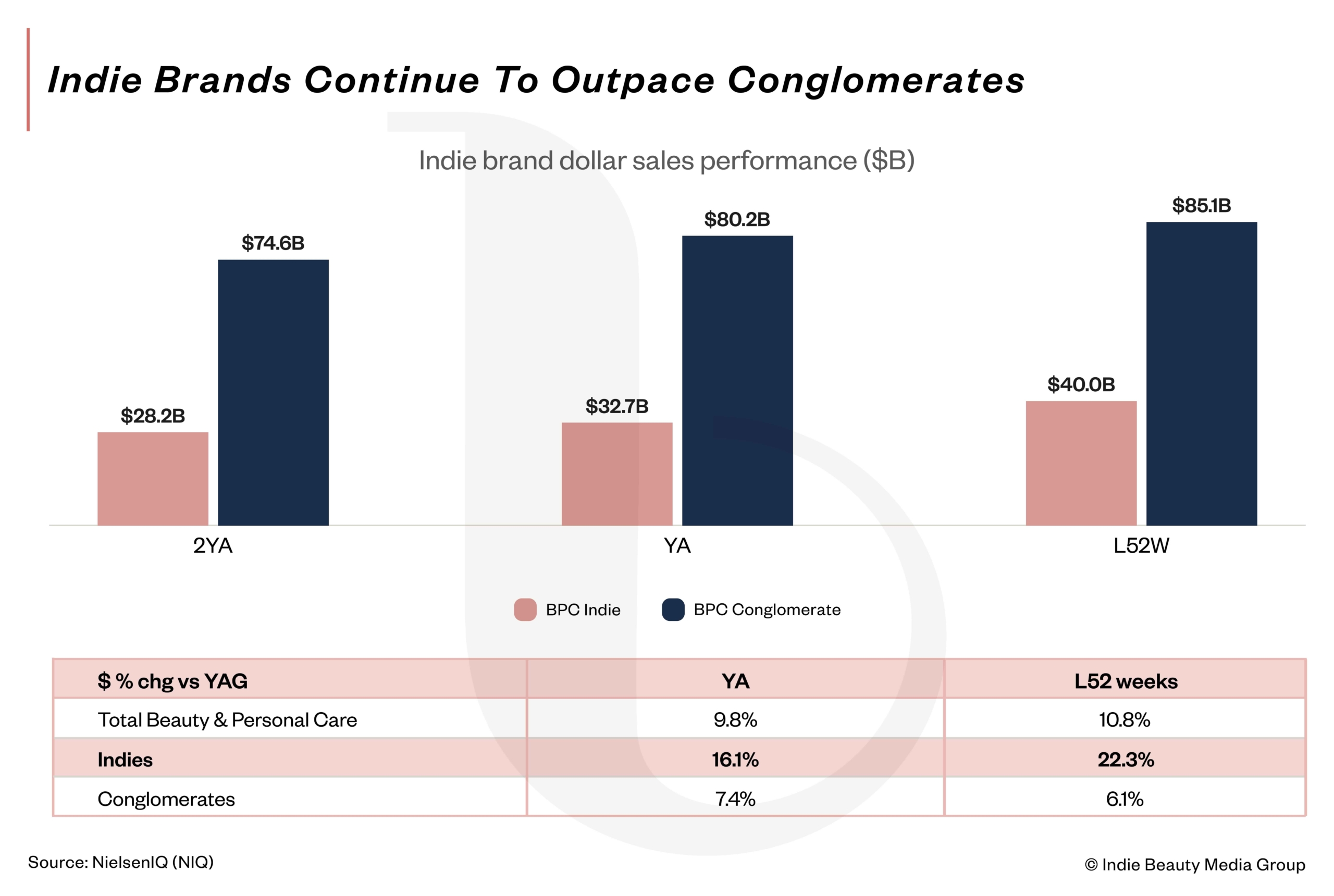

According to new data from NielsenIQ, indie brands controlled about 32% of the $125 billion U.S. beauty and personal care market in the latest 52-week period ended Nov. 1, 2025, up from roughly 29% a year earlier. Indie brands are hastening their encroachment on conglomerate turf by growing 22.3%, compared with 6.1% for conglomerates. In the prior 52-week period, indie growth was 16.1% versus 7.4% for conglomerates.

The divergence is rooted in how growth is being generated. Indies are boosting volume through more visits, while conglomerates are relying more on price increases. Specifically, 62% of indie beauty dollar growth stems from more shopping trips, and 64% of conglomerate dollar growth stems from price increases. Anna Mayo, VP of the beauty vertical at NIQ, says, “Indies tend to do better among those enthusiasts who really want to experiment.”

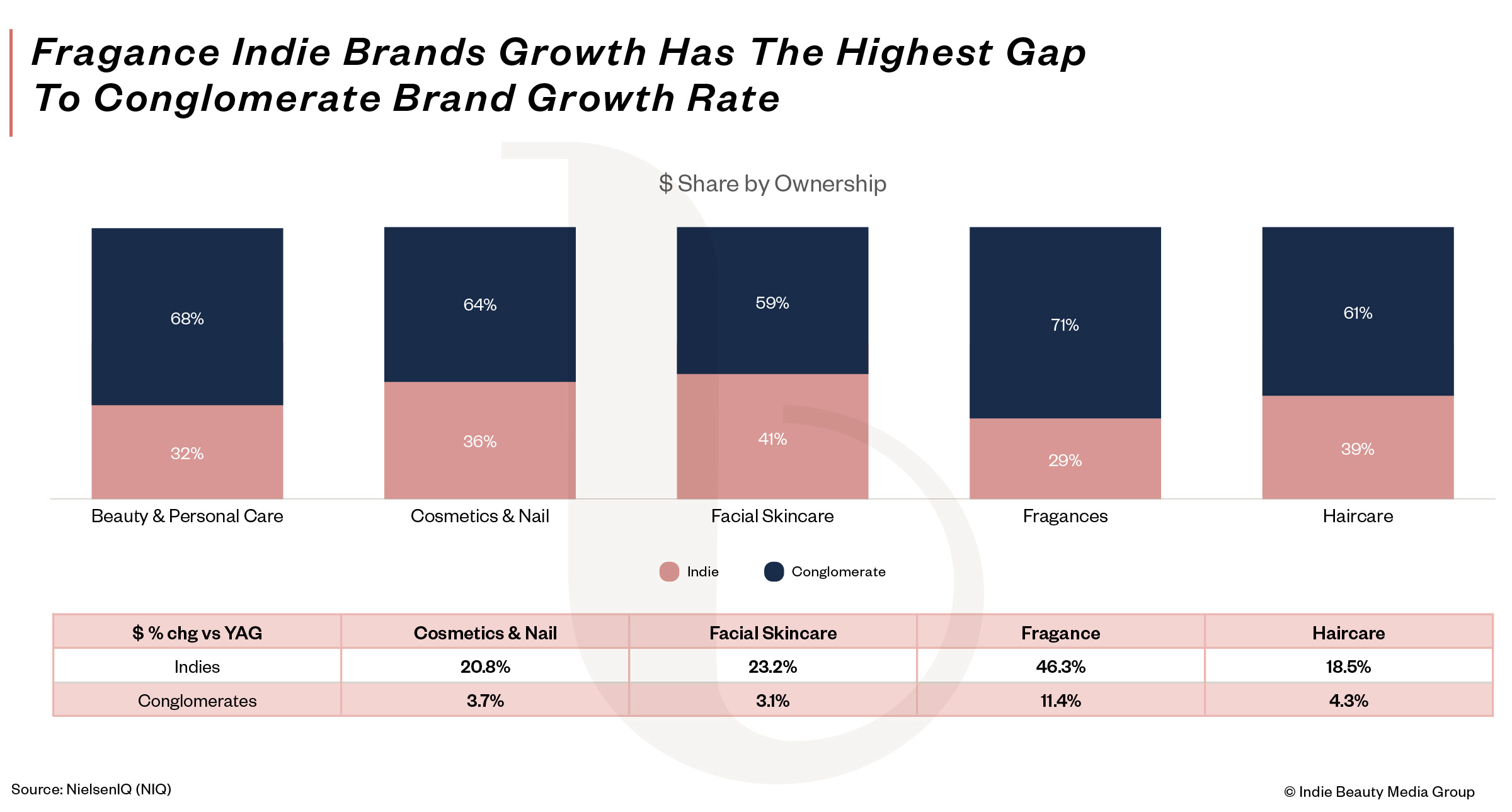

Indie beauty’s penetration and growth vary by category. In the latest 52-week period, indie fragrance sales surged 46.3%, compared with 11.4% for conglomerates, even as conglomerates maintained the lion’s share of the category, at 71% to indies’ 29%. In facial skincare, indie sales jumped 23.2% against 3.1% for conglomerates, with indie brands accounting for about 41% of category sales.

In cosmetics and nail, indie sales increased 20.8%, compared with 3.7% for conglomerates, giving indies roughly 36% of the category. Haircare showed a narrower disparity, with indie sales climbing 18.5% versus 4.3% for conglomerates, and emerging brands representing about 39% of the category.

The picture isn’t entirely rosy for indie beauty. Mayo points out a loyalty gap favors conglomerate brands, which benefit from stronger repeat purchasing and a commanding lead in retail shelf space, and churn in the market is accelerating, with once-hot upstarts often cooling quickly as the next viral brand is knighted by algorithms.

NielsenIQ’s data shows a 4.4-point loyalty divide, with conglomerate brands registering an average loyalty score of 13.2 versus 8.8 for indies, a measure of how often the average shopper returns to buy from the same brand over a 52-week period. At mass retail, conglomerates claim 2.8X the distribution of cosmetics and nail indie brands, 2.6X in facial skincare, 1.9X in haircare and 1.4X in fragrance.

“It is an easier environment than ever right now for a brand to get trial. People are really willing to try new things to test out, but the flip side of that is that there’s always something new to try,” says Mayo. “So, it’s harder than ever to get people to come back. That’s what a lot of indie brands have to fight with. It’s how do you make sure that your product is constantly innovating or being exciting enough that make that shopper who’s really experimental and liking to try the latest and greatest to get them to come back.”

NIQ has broadened its definition of indie beauty brands to encompass companies generating up to $300 million in annual revenue, up from $200 million, a shift that reflects the rise of bigger, fast-growing brands not owned by major conglomerates and may influence year-over-year comparisons. Laura Geller Beauty and Medicube are examples of brands captured under the wider definition.

The change added eight brands and about $1.9 billion in sales to the indie beauty total over the latest 52-week period. NIQ tracks 2,199 indie beauty brands, including 18 generating $100 million to $200 million in annual sales, 39 generating $50 million to $100 million and 2,134 generating $1 million to $50 million. Brands below $1 million in annual sales are excluded from NIQ’s indie beauty dataset.

Amazon and e-commerce are critical propellants of indie beauty growth. Amazon is the largest beauty retailer, with an estimated 22.7% share of U.S. beauty sales, roughly on par with the mass retail channel as a whole. E-commerce accounts for about 48% of total beauty sales and 70% of indie beauty sales. It’s growing 22%, compared with 2% for in-store. Mayo forecasts the beauty industry could reach parity between online and offline sales by the end of the year, pulling forward her earlier three-to-five-year forecast.

“We’re just seeing Amazon really take over what beauty means…The big growth drivers of beauty retail have been Amazon and TikTok Shop. They’ve become the default channel in people’s minds, where they’ve done what I like to call a focus on the boring business basics,” says Mayo. “TikTok Shop has been a really important discovery engine, so even brands that are not necessarily converting a lot of sales on TikTok Shop are still seeing it as an important driver of brand awareness.”

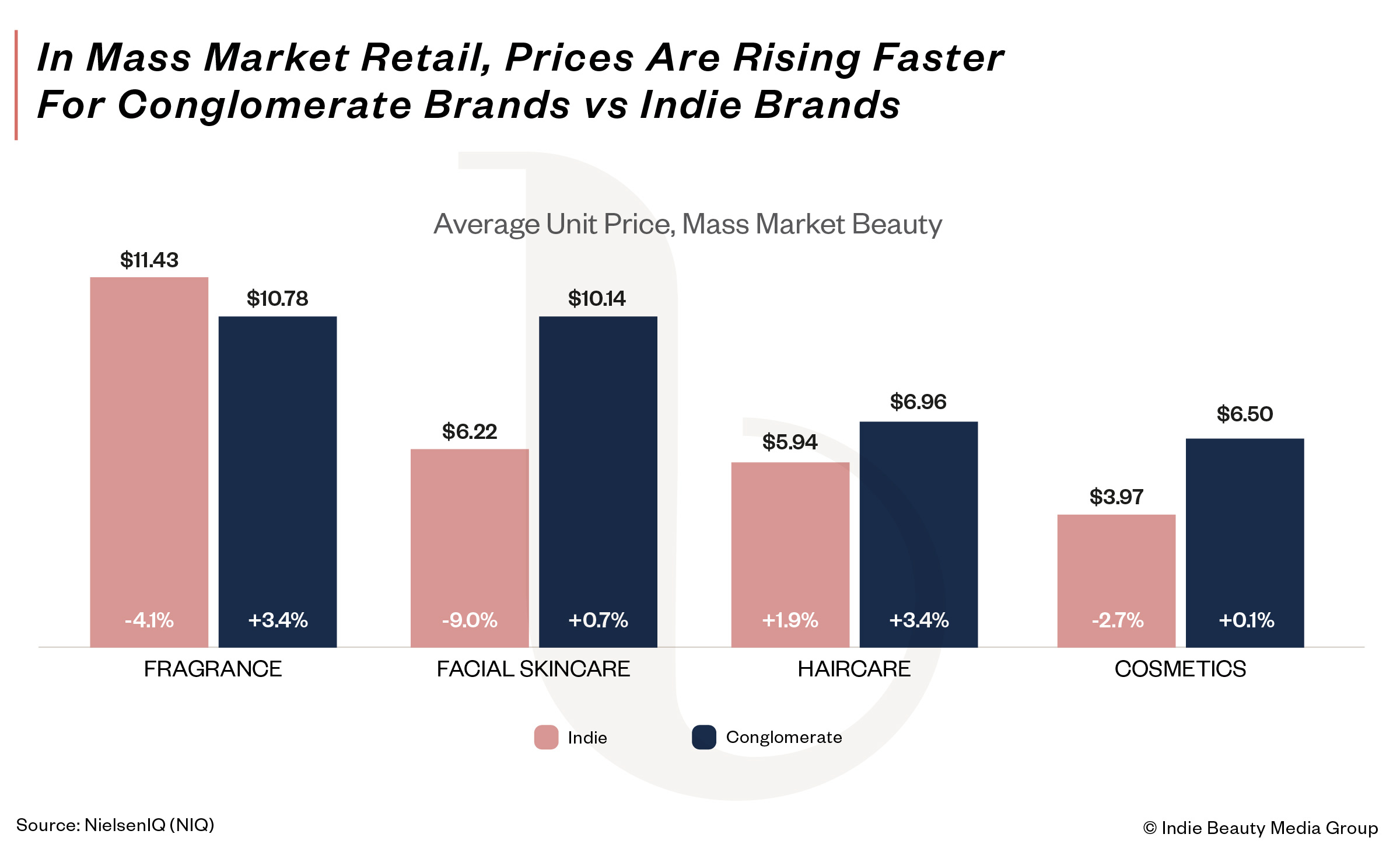

A surprising dynamic in indie beauty’s challenge to conglomerates is pricing. While smaller brands often face a heavier burden from cost pressures, NIQ reveals that, in mass market retail, conglomerate brands have raised prices faster than indies, reversing the conventional assumption. In mass retail, indie brands posted price declines in fragrance (-4.1%) and cosmetics (-2.7%) and modest increases in facial skincare (+1.9%) and haircare (+3.4%), while conglomerates recorded gains across all four segments, led by fragrance (+3.4%) and haircare (+3.4%).

“There is this assumption that indies are always higher priced, and I don’t think it’s necessarily true, and they also are not raising their prices higher,” says Mayo. “There’s been all this talk about tariffs hitting indies harder. I think conglomerate brands are better at managing their pricing and reacting to pricing in a way that consumers are ready for, and indies have been a little more reluctant to raise prices.”

Mayo explains the pricing dynamic aligns with a K-shaped economy, with high-income consumers driving a disproportionate share of beauty spending. Households earning more than $100,000 a year account for nearly half of beauty spending and are growing 18% to 20% year over year. Lower-income consumers making under $50,000 represent about a quarter of sales and are flat to slightly declining in their spending.

Across the market, beauty prices have remained relatively stable despite tariff-related cost hikes. NIQ data shows they rose about 3% in the latest period, with demand remaining resilient. “If you raise prices, people are not likely to step away,” says Mayo. “The price isn’t as much of a barrier.”

As indie beauty brands grow amid intense competition for attention, the key test will be whether they can build the scale, systems and customer economics that make them attractive acquisition targets or formidable enough to stay independent. For conglomerates, the imperative will be to engineer trial for existing brands or use M&A to fuel it.

“It doesn’t mean that every indie brand is going to have staying power…We’re going to continue to see a lot of brands come and go. The brand that was hot last year doesn’t mean it’s still growing this year,” says Mayo. “As these brands get bigger and as they have bigger aspirations, they are going to need to nurture their customers a little bit more. And I think paying more attention to, do we have the right assortment at the right retailers? Do we have the right prices? These questions are maybe not as fun for a founder to be tackling, but that’s how brands get big and stay big.”

Leave a Reply

You must be logged in to post a comment.