The DTC brand is dead. Long live the DTC brand.

Advent International has acquired Salt & Stone, the premium body care brand that underscores how an evolved direct-to-consumer model spanning retail, Amazon and owned channels can drive significant value.

Terms of the deal, slated to close in April, weren’t disclosed, but Drew Fallon, CEO and co-founder of financial planning platform Iris Finance, estimates the price at over $500 million based on comparable transactions, implying a roughly 3X multiple on $165 million in sales last year, when the brand posted double-digit growth across its distribution. Founded in 2017 with mineral sunscreen by former professional snowboarder Nima Jalali, whose knee injury prompted him to seek better-for-you products, Salt & Stone generates 40% of its sales from DTC, while deodorant accounts for around 40% of its business and sells every five seconds.

“What’s always stood out to me about this brand is how founder-led curiosity can be such a powerful entry point. Nima didn’t come from traditional beauty, and I actually think that’s part of what made the brand so compelling,” says beauty investor Manica Blain, founder of Top Knot Ventures. “A former pro snowboarder starting a brand in sunscreen and then evolving into body care and fragrance felt very instinctive rather than over-engineered. Sometimes the best brands are built by consumers who are just deeply attuned to what they themselves want but can’t find.”

Jaime Schmidt, investor at Color Capital and founder of Schmidt’s Naturals, the deodorant brand that sold to Unilever in 2017, says, “Investors still see real opportunity in personal care when a brand has a distinct point of view and room to grow beyond one standout product, but the bar is higher now. It’s not enough to just be a disruptor in a legacy category. The brands that stand out are the ones that feel differentiated enough to matter and durable enough to keep growing.”

Salt & Stone follows brands like Phlur, Supergoop, Briogeo and Drunk Elephant through the Sephora-to-exit pipeline, but its trajectory diverges in key ways. The Los Angeles brand entered Sephora internationally first, launching in the United Kingdom, Australia and Southeast Asia in 2023 before arriving in the United States in 2024. Salt & Stone has the No. 1 deodorant at Sephora in the U.S.

“Nima and the team were deliberate about building real consumer demand, the kind that shows up in repurchase rates and organic word-of-mouth, before stepping into the most competitive retail doors. That patience is increasingly rare, and it’s exactly what makes a brand attractive to a PE firm like Advent,” says Daniel Faierman, partner at investment firm Habitat Partners. “We regularly see brands trying to get into Sephora ASAP before ample brand awareness, aka mental distribution, is built. This deal also signals that the Amazon-plus-specialty retail combination is no longer a contradiction.”

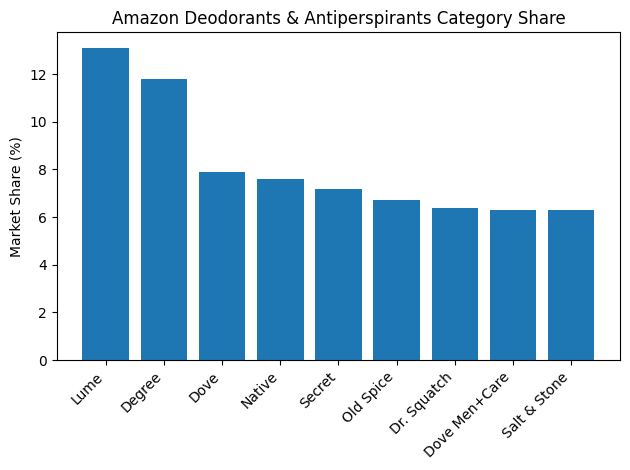

Perhaps to the chagrin of Sephora executives eager to keep its brands off Amazon, that contradiction is being unraveled as the e-commerce giant has been a linchpin of Salt & Stone’s success. According to commerce growth agency Navigo Marketing, the brand holds the No. 1 bestseller rank for its hero aluminum-free deodorant in the scent Santal & Vetiver, commanding a 6.3% share of sales in Amazon’s deodorant and antiperspirant category and ranking ninth overall. Its competitors on Amazon include mass-market brands such as Lume, Degree, Dove and Native.

“The brand has effectively built premium authority in a category where most players compete on price.”

Navigo finds that the brand draws around 343,000 monthly searches on Amazon and its search visibility has doubled year over year, exceptional for a premium brand and indicating strong consumer awareness and repeat purchase behavior. Salt & Stone’s core customers skew millennial. Navigo underscores that, rather than dispersing into dozens of products, Salt & Stone’s sales are concentrated in a small number of A-level products, propelling algorithmic favor and review consolidation on Amazon.

“The brand has effectively built premium authority in a category where most players compete on price,” says Meredith Matthes, account director at Navigo. She adds, “The deodorant category on Amazon is one of the most competitive in personal care, with legacy brands spending tens of millions to defend their share. The fact that Salt & Stone carved out a top-10 position at nearly double the average price tells you something meaningful about where the consumer is headed.”

Shamin Walsh, managing director at BAM Ventures, says Advent’s Salt & Stone deal “demonstrates continued validation of the consumer wedge between premium and budget. People who can spend continue to spend with seeming price inelasticity and don’t weigh purchases purely transactionally. They’re not thinking, ‘I could get the same functionality at half the cost.’ They’re buying into a product and brand they enjoy, and the incremental cost is somewhat immaterial to them…Smart brands build their distribution around existing customer behavior rather than trying to redirect it. Body care is an easy cart add-on when you’re already shopping, so it makes a lot of sense to prioritize in-retail and Amazon as channels.”

Salt & Stone’s traction is evidence of the premiumization of traditionally commoditized categories like deodorant and body care. On Amazon, Navigo approximates that Salt & Stone’s average selling price is $37.01 versus a category average of $20.34. Salt & Stone’s scents, developed with DSM-Firmenich, and its natural ingredients have been important growth catalysts for the brand at a moment of fragrance frenzy and ingredient concerns. Although there’s a backlash to the movement away from aluminum in certain beauty circles, the aluminum-free deodorant segment has been accelerating 1.5X to 2X faster than the overall deodorant category.

Up and down the value chain in the segment, if the premiumization persists, it could have widespread implications for future dealmaking. Other brands in the body care and deodorant arena that industry insiders are watching include Athena Club, Evolvetogether, Corpus, Hanni, Nopalera, AKT London, Curie, Nécessaire and Kaia Naturals.

“Salt & Stone’s acquisition shows that functional luxury in body care is here to stay. I think that this deal proves there’s massive appetite for elevated body care from consumers, but it also highlights the gap we’re filling, and I feel very excited that it is shining a light on the category,” says Mary Futher, founder of Kaia Naturals. “I also feel that it is showing the investment community that premium body care is no longer a small niche category. I see this as something very positive, and I think you will find more acquisitions in this area.”

Schmidt believes Advent’s acquisition of Salt & Stone represents the category moving to a different phase. “Early on, the opportunity was to prove that deodorant could be rethought and elevated,” she says. “Now the question is which brands can actually hold onto consumer attention and become enduring businesses.”

Among the largest beauty deals so far this year, which have included Chillhouse’s sale to Kiss Beauty Group, RoundTable Healthcare Partners’ acquisition of Colorescience and Henkel’s purchase of Not Your Mother’s, investors hope Advent’s acquisition of Salt & Stone can help break an M&A logjam. Last year, beauty deal activity declined slightly, although several blockbuster transactions occurred, notably E.l.f. Beauty’s acquisition of Rhode and L’Oréal’s deal tied to Kering’s beauty properties. Marquee assets have been trading at roughly 12X to 20X earnings before interest, taxes, depreciation and amortization (EBITDA), with mid-tier assets closer to 8X to 12X EBITDA.

“This deal proves there’s massive appetite for elevated body care from consumers.”

“Health and beauty has been beaten up for the past 18 months for God-knows-what reason,” says Mike Duda, managing partner at investment firm and creative agency Bullish. “The Advent deal for Salt & Stone could very well reverse the macro dip the category has had, sans one-offs like Rhode, and could send multiples back up.”

Salt & Stone raised capital from Humble Growth, backer of Fruit Riot, Momentous, Urbanic and Eez, in 2024 prior to its sale to Advent, with Humble Growth selling its stake in the transaction. Advent’s beauty M&A track record is mixed. The firm invested in Olaplex in 2020, and the haircare company’s public offering in 2021 marked one of the most lucrative beauty investments ever. However, Advent has stumbled with Orveon, a platform company with Bare Minerals, Buxom and Laura Mercier in its stable. Currently, the firm’s portfolio includes Orveon, Skala Cosméticos, Parfums de Marly and Initio Parfums Privés.

With Salt & Stone’s sale to Advent, Jalali will retain a leadership role and remains an equity holder. The brand has been hiring beauty veterans of late, and they will be integral to its next chapter. Meagan Rosson, previously CFO of Tula Skincare, is president, and Abby Tellam, previously VP of integrated marketing at Wyn Beauty and director of brand marketing at Glossier, is CMO. Chris Elshaw, ex-COO of Revlon and former chair of Paula’s Choice, Medik8 and Orveon, will chair Salt & Stone’s board.

Two aspects of Salt & Stone’s rise in particular pique Blain’s interest: the speed of Humble Growth’s liquidity event and the rumored secondary structure of its deal with Salt & Stone. In a secondary transaction, investors purchase shares from existing shareholders rather than injecting new capital into the business.

Discussing speedy path to a deal post-Humble Growth investment, Blain says, “There’s a growing recognition that, if you have the opportunity for a strong outcome, even if it’s earlier than expected, it can be the right move. Not every brand needs to be held indefinitely in pursuit of a perfect outcome, especially in a market where timing and momentum matter as much as scale.”

She expects secondary transactions will mount in the consumer space, but on a selective basis involving founders with protracted stays at their companies and brands with real product-market fit, healthy unit economics and a level of predictability in their models.

“For founders who have been building for years, often with very little liquidity along the way, secondary can be quietly transformative,” says Blain. “It allows them to take some capital off the table and, in doing so, remove a layer of existential pressure that sits behind every decision. When your entire net worth is tied up in the business, the stakes can become so high that it actually constrains decision-making.”

Click here to learn more about Beauty Independent’s Dealmaker Summit running June 8 to 9 in New York.