Beauty is being injected with med-spa marketing.

Read a recently launched topical skincare product description page today and you may feel like you’re researching an aesthetic procedure rather than a serum. From drugstore brands like Olay to premium skincare specialists like Plated, procedure-adjacent skincare products marketed as needle-free fillers, collagen stimulators without in-office injections, PDRN skin boosters without downtime and lifting products echoing the vocabulary of facelifts and threads are on the rise.

The topical skincare at Sephora is increasingly being sold less as subtle enhancements and more as aesthetic medicine’s at-home extension, borrowing the language of med-spa procedures to promise visible results without needles, lasers or downtime. Amy Peterson, medical esthetician, founder of Miami aesthetic clinic Skincare by Amy Petersen and luxury clinical skincare brand Lenox and Sixteenth, says, “The aesthetic treatment room has become a reference point for results. Consumers today understand what lasers, microneedling and energy-based devices are designed to do, so that language has become a clear way for brands to communicate efficacy.”

That feedback loop between consumer and company is in full flow. According to marketing agency Front Row’s Amazon Beauty Category Snapshot for the first quarter of 2026, searches on the platform saw spikes in “longevity” and “cellular repair” skincare. Demand for “faux-tox” and non-invasive alternatives delivering results at home is soaring, with search volume for “volufiline serum,” up 3,829% year-to-date and “instant face lift serum” seeing over 437,000 searches year-to-date. Front Row asserts, “Shoppers aren’t just buying moisturizer, they’re researching cellular repair.”

There are four popular procedures that seem to be especially inspiring to topical skincare brands.

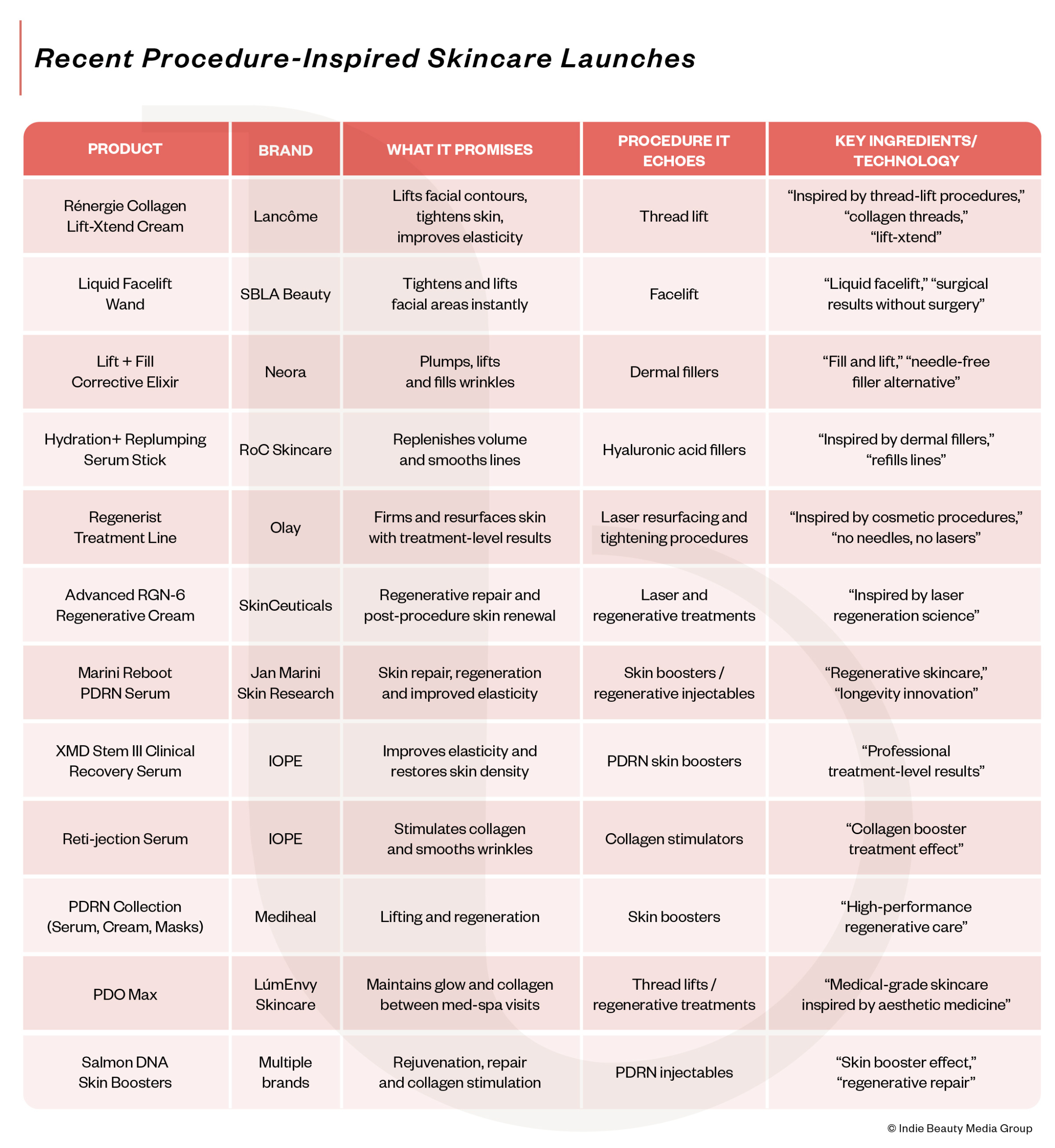

1. Thread-Lift-Inspired Skincare

These products emphasize lifting, tightening and contour repositioning. The thread lift analogy works well because it communicates instant structural change, even if the mechanism is purely topical. An example of a product inspired by thread-lift benefits is Lancôme Rénergie Lift-Xtend.

2. Filler-Inspired Skincare

These formulas target volume loss, which is increasingly recognized as a core result of aging. Marketing focuses on plumping, volume restoration and deep line smoothing. An example is RoC’s Hydration+ Plumping Serum.

3. Biostimulator-Inspired Skincare

This category borrows language from injectables that stimulate collagen production such as Sculptra or skin boosters. Common claims from these products include collagen stimulation, skin regeneration and elasticity recovery. An example is IOPE’s Reti-jection Serum.

4. Post-Procedure Care-Inspired Skincare

These products position themselves as supportive care after aesthetic treatments rather than replacements for those treatments. Typical messaging is around recovery, extending results between treatments and clinical-grade maintenance. An example is LúmEnvy Skincare PDO Max.

Peterson contends that these claims may not be outlandish. She says, “The right ingredients can strengthen the barrier, support collagen pathways, improve brightness and refine texture over time. When those foundations are in place, professional treatments tend to perform better, and their results are often more sustained.”

The Clinicalization Of Skincare Marketing

Across new topical skincare launches, marketing vocabulary is shifting toward the language of aesthetic medicine. Instead of promising vague anti-aging benefits, brands are now using terms associated with clinical procedures. Structural words like “regenerate” are replacing traditional beauty language and procedural comparisons like “thread-lift effect” are appearing more explicitly.

This strategy taps into growing consumer familiarity with aesthetic treatments such as fillers, neurotoxins, biostimulators, thread lifts and skin boosters, while positioning skincare as a lower-risk entry point or maintenance step between clinic visits. In general, skincare marketing language is moving in four noticeable directions:

- From anti-aging effects to intervention-esque.

Brands are no longer just saying a serum “firms” or “smoothes.” They are dubbing these topicals as “procedure-inspired,” “treatment-level,” “approved by plastic surgeons” and a “first step” or “in-between step” for people considering in-office treatments. - From wrinkle reduction to structural vocabulary.

The newest phrasing discusses volume loss, contour, lifting, plumping, collagen support, resilience and recovery. This language mirrors injectable indications and in-office device consults, not legacy skincare copy. - From pampering products to zero-downtime efficacy.

A big part of these products’ pitches is convenience: professional-level results “without invasive procedures,” “without downtime” or “without discomfort.” - From beauty boosts to regenerative medicine lite.

PDRN, exosomes, laser skin regeneration science and longevity all point to topical skincare vying to create a halo effect and legitimacy from medical aesthetics and biotech.

Clinical Skincare Drives Beauty Deal Flow

The med-spa-ification of skincare is unfolding as the aesthetics space outpaces traditional beauty categories. The U.S. medical spa market is projected to advance at a roughly 13.8% compound annual growth rate through 2030, according to Grand View Research, far above the low- to mid-single-digit growth rates typical of the beauty industry. A recent survey from Boston Consulting Group and Women’s Wear Daily found consumers are expanding their beauty routines beyond skincare and makeup into aesthetic procedures and performance-focused wellness, with a highly engaged segment of roughly 15 million Americans viewing such treatments as part of a broader “system of care.”

Investors and strategic buyers have long gravitated toward skincare brands with clinical positioning and professional-channel credibility. The trend dates back at least to L’Oréal’s acquisition of SkinCeuticals in 2005, but deal activity has accelerated in recent years with transactions including Waldencast’s acquisition of Obagi, Galderma’s purchase of Alastin and L’Oréal’s takeover of Skinbetter Science.

Earlier this year, brand holding company KYT Group acquired plastic surgeon-founded Glo Skin Beauty and L’Oréal acquired Medik8. Professional acne specialist Phyla has secured $9 million from investors, including LIFT Ventures, while Epicutis raised $10 million in series B funding last year.

According to a report last year from venture capital firm XRC Ventures, 26% of VC funding in beauty and personal care went to science-backed or clinically validated brands in 2024, up from 17% on average in the prior five years. XRC also found science-backed skincare brands have traded at revenue multiples roughly 20% higher than brands without clinical positioning, with biotechnology-focused brands commanding even higher premiums.

Separately, market research firm Kline & Co. recently identified numerous science-centered and professional skincare brands among its most likely indie beauty acquisition targets, including Ourself, 111Skin, Plated and Dr. Diamond’s Metacine. In April, Estée Lauder announced it had taken a minority stake in 111Skin.

Leave a Reply

You must be logged in to post a comment.