Like many in the Ozempic era, Unilever is parting with food to focus on beauty.

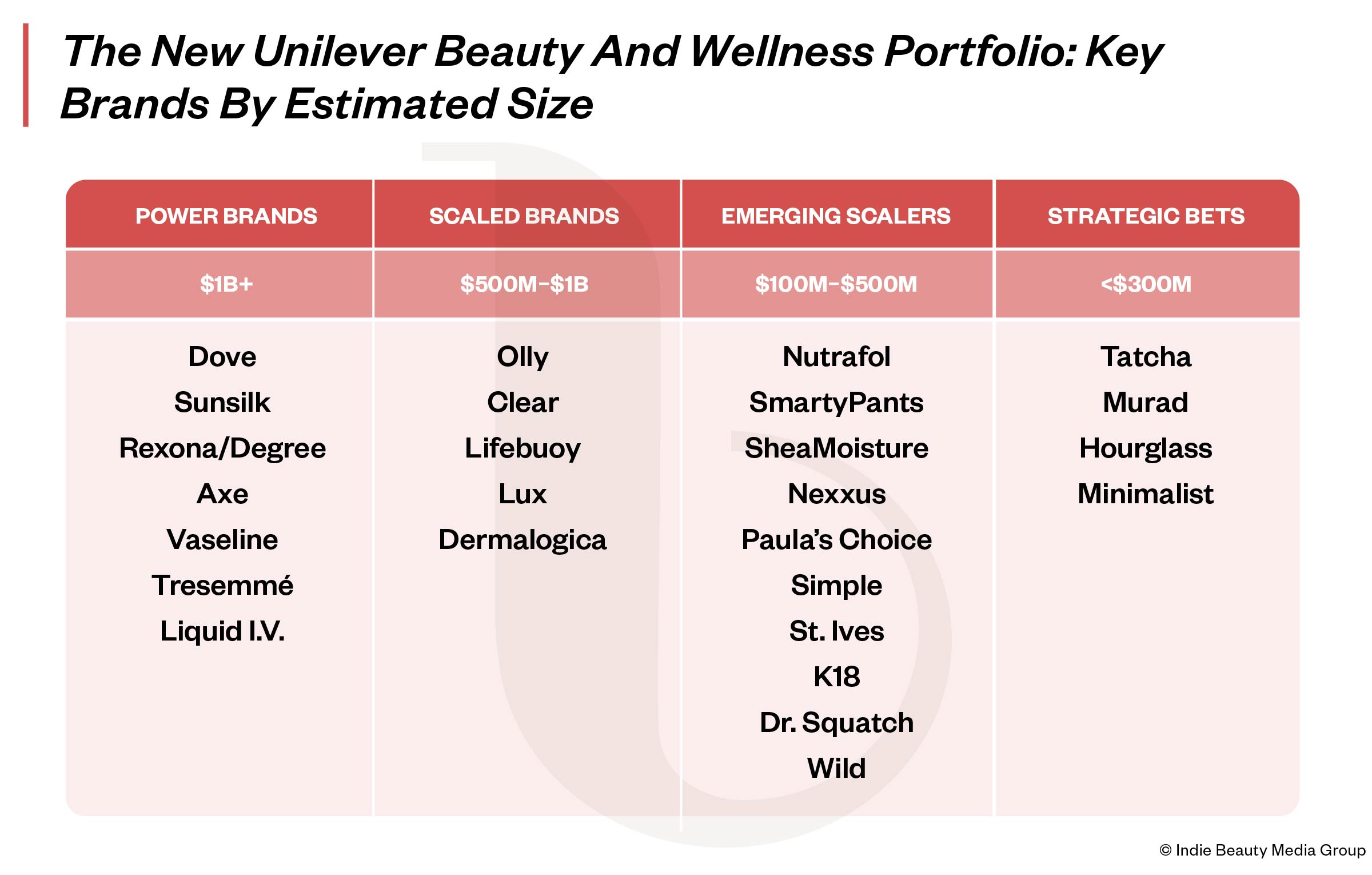

The consumer goods conglomerate’s roughly $65 billion transaction exiting its approximately $14 billion food business to McCormick & Company unwinds the marriage of the two industries that birthed it in 1930 with the merger of Margarine Unie and Lever Brothers. What will result is an around $46 billion beauty- and wellness-centered company, second only to L’Oréal in beauty, with faster growth, significant share in core categories and the potential to expand further across both emerging and developed markets.

But it also has notable gaps as it contends with competitors, both entrenched and emerging. Unilever remains heavily weighted toward mass, a strength as consumers seek value, but not without risk as K-shaped dynamics widen the divide between haves and have-nots. In a recent article in Business of Fashion, fragrance and color cosmetics are identified as weaknesses for Unilever.

Unilever hasn’t hesitated to pull the M&A lever to address its weaknesses and seize growth opportunities. The company allocates roughly $1.7 billion annually to acquisitions and is set to receive about $15.7 billion in cash from the McCormick deal that could be redeployed into beauty and wellness.

In the past three years, it has acquired brands such as Grüns, Wild, Dr. Squatch, K18 and Minimalist, while divesting or shuttering Kate Somerville, Suave, Ren Clean Skincare, Dollar Shave Club and the Elida portfolio. It’s also invested more than an estimated $360 million in Indian beauty brands since 2023, including Clayco, Secret Alchemist, SkinInspired and RAS Luxury Skincare.

As beauty and wellness welcomes its newest pure-play operator, industry watchers are considering what it could mean for dealmaking and the indie-to-exit pipeline. To explore the possibilities, for the latest edition of our ongoing series posing questions relevant to indie beauty, we asked nine investors, consultants and marketers the following: If you were leading Unilever’s M&A strategy today, where would you direct investment and why? Are there specific beauty or wellness brands you believe would be strong fits for the company? How might a beauty and wellness-led Unilever reshape the beauty ecosystem, particularly for emerging brands?

-

Tracy Gehrmann Co-Founder, TNGE

Tracy Gehrmann Co-Founder, TNGE Unilever has overpaid for brand heat before and has the divestitures to show for it. The filter going forward is different: find businesses where the product commands the premium, not the brand.

That means one type of company specifically: science-led brands with genuine clinical differentiation, high repurchase rates and a consumer who comes back because the product works, not because the founder is compelling on TikTok.

Nutrafol, Liquid IV, Grüns. These are businesses built on efficacy and habit, not a fleeting aesthetic. And Unilever has shown recently that they can scale these post-acquisition.

On categories, functional wellness is the clearest priority: sleep, gut health, hydration, cognitive performance as well as skin- and scalp-first beauty. Fragrance and color cosmetics are the obvious gaps in their portfolio on the beauty side, but social-first plays with trend-dependent velocity are not the fit.

Unilever doesn't win by building brands from culture. It wins by taking something with proven science and real retention and pushing it through infrastructure most indie brands could never access.

For emerging brands, the entry ticket is narrow: strong retention metrics and a product USP that doesn't depend on the founder being in the room. Brand narrative alone won't get you to the table.

The $15 billion coming off the food sale will move the market, but the challenge is to deploy it well. Most acquisitions destroy value. That's the historical record.

Valuations have deflated in recent years, which created real opportunities for inorganic growth, but windows close fast when the right assets attract competition. The answer is fewer, higher-conviction bets: go earlier on high-growth assets that fit the strategy, anchor the portfolio with established players that have already proven longevity across economic cycles.

- Rachel Hirsch Founder and General Partner, Wellness Growth Ventures

What makes Unilever's position uniquely interesting is how active they've been on both sides of the ledger. Most conglomerates acquire. Fewer have the conviction to simultaneously divest and do it at volume.

The willingness to cut Kate Somerville, Ren, Dollar Shave Club and the Elida portfolio while bringing in K18, Minimalist and Dr. Squatch in the same window is a level of portfolio discipline you don't see often.

L'Oréal operates with similar intentionality, but across the broader conglomerate landscape. This kind of active two-way dealmaking is rare. It signals a company that actually has a point of view on what it's building, not just what it can afford to buy.

If I were leading Unilever's M&A strategy right now, I'd be thinking about three things: filling the category gaps, winning the channels of the future and betting on the science-backed wellness convergence that's eating legacy beauty.

Fill the obvious hole: fragrance. Unilever's fragrance portfolio is largely functional (Dove, Axe) rather than aspirational. In a world where fragrance is having a genuine cultural moment, and gen Z treating scent as identity, not hygiene, that's a real miss. I'd be looking at indie fragrance brands with cult followings and margin profiles that make sense at scale.

Double down on the science-wellness convergence. K18 shows they understand this. The next wave is brands sitting at the intersection of longevity, skin health and body composition.

Think topical peptides, collagen-adjacent skincare, products built around the GLP-1 consumer (muscle retention, skin elasticity shifts, body recomposition). This is where I'd be most aggressive. A beauty-wellness Unilever should own the science-backed body category before Estée Lauder or L'Oréal gets there.

Go deep on the menopause and midlife woman, the most underserved, highest-spending consumer in beauty and wellness. Brands building specifically for hormonal skin changes, thinning hair and the longevity-focused 45 to 60 demo are still largely indie. Unilever has the distribution to take one of these to scale globally, and almost no one at the conglomerate level has credibly claimed this white space yet.

What I'd avoid: celebrity brands at inflated multiples, anything dependent on a single hero SKU without clinical backing and mass color competing directly with E.l.f. on price.

The broader ecosystem implication is real. A beauty-and-wellness Unilever with $15 billion-plus in fresh capital and a mandate to grow raises the floor for what indie brands can exit into. But founders should be clear-eyed. This is a performance-driven acquirer, not a brand museum. They've proven they'll cut what doesn't fit.

- Tina Bou-Saba Founder and Managing Partner, CXT Investments

I joke that “wellness is eating the world,” and Unilever’s divestment of its food business to focus exclusively on beauty and wellness is a perfect example of this movement. I think that it’s a brilliant move. Generate liquidity through the food business sale in order to focus the corporation on the faster-growing and more profitable personal care category.

Presumably a meaningful portion of the $15.7 billion in cash from the McCormick deal will be used to support M&A, as we already saw with the Grüns acquisition and investment in existing brands like Dr. Squatch and Nutrafol, as well as the recently acquired Indian beauty brands, which appear to have strong potential.

If I were leading Unilever’s M&A strategy today, I would feel fortunate to have one of the coolest jobs out there! I believe that there is tremendous opportunity here to build a modern conglomerate that is focused squarely on the consumer trends that will define the next decade and beyond.

At the risk of sounding dramatic, I believe that wellness and AI are by far the two most important forces driving the consumer industry. Unilever is wise to be doubling down on the former.

Moreover, I believe that the company has a solid track record as an acquirer. Brands like Nutrafol and Liquid I.V. have been home runs, for example. Dollar Shave was less successful, but I expect that management has learned a lot from its wins and losses in this department. A bit cynically, Unilever likely has a unique window of opportunity while Lauder is distracted by its Puig deal and subsequent integration (why?!), and its only major competitor for big beauty deals is L’Oréal.

In that hypothetical role, I would look at acquisition opportunities through a number of lenses, including category, tier, distribution (both channel and geography), size, brand and community and product. If Unilever generally sticks to its $1.7 billion annual acquisition allocation, then perhaps in a typical year we will have $1 billion deal (like Gruns, Nutrafol, and Squatch) and one or two smaller ones.

Of course, this is not an exact science, but the point is Unilever will likely be acquiring companies for a few hundred million to ~$1.5 billion at the high end. This already tells us a lot about the size of brands that they might acquire.

I’d love to see Unilever pick up a scaled prestige clean color brand like Kosas or Saie (disclaimer: I am an investor in both) that is strong in community, product development and digital/social. “Clean beauty” is no longer a buzzword, but is rather a key contributor to skin (and overall) health for many consumers, and thus aligns beautifully with Unilever’s wellness focus.

Likewise, Arrae and Needed (both of which I am an investor in) would elegantly complement existing supplement brands like Nutrafol and Gruns by thoughtfully addressing specific consumer communities with high-integrity and effective products. Fragrance and prestige haircare represent compelling opportunities as well, and there are a number of strong assets in both categories that could be future targets.

With respect to the broader beauty ecosystem, Unilever’s strategy is certainly positive. The corporation is focused, and it has cash to spend on acquisitions.

However, I expect that Unilever will be highly attentive to the financial profile of potential acquisitions, specifically, scale, gross margins, overall profitability, unit economics and other key financial metrics. In other words, they likely will be looking for healthy businesses with global distribution potential, certainly not growth-at-all-costs brands with upside-down P&Ls.

In the near to medium term, I don’t expect that this will reshape the beauty ecosystem. However, over the longer term, it may push beauty competitors to embrace wellness categories like supplements, which historically have been out of scope for traditional beauty conglomerates.

- Asha Talwar Coco Founder and CEO, GlowUp Partners

Unilever walked away from prestige fragrance in 2005. I was there. They sold Calvin Klein, Chloe and Vera Wang to Coty for $800 million because the category felt mature. Nobody anticipated fragrance becoming the fastest-growing segment in prestige beauty. It is now supercharged by its intersection with wellness and neuroscience, with scent a tool for mood, memory and mental well-being. It is increasingly the hottest category in M&A, with L'Oréal's $4.7 billion Creed deal signaling just how fiercely conglomerates are competing for the best assets.

With $15.7 billion to redeploy, that is the category I would re-enter first. There are founder-built niche houses with devoted communities, credible wellness positioning and significant international runway that would be strong fits. The founders who benefit most from this new Unilever will be the ones who got the fundamentals right before they went looking for a buyer. The company buys proven models, not promising concepts.

- Nicole Fourgoux Operating Partner, Stride Consumer Partners

Unilever’s strategic direction is closely aligned with where the most powerful growth drivers in beauty are today. Management has been clear about its priorities: increasing exposure to beauty and well-being and personal care, premiumizing the portfolio and leaning into digital channels and higher-growth markets such as the U.S. and India, supported by a disciplined, bolt-on approach to M&A rather than large-scale transformation.

This strategy maps directly against a set of structural shifts in beauty consumption that continue to drive outperformance.

First, the convergence of beauty, health and wellness, increasingly framed through a longevity lens, but also through the skinification of hair and makeup, is expanding the category beyond traditional definitions. This is visible in both outside-in formats such as biotech skincare and inside-out solutions such as supplements, as consumers increasingly look to address beauty at a biological level.

Second, consumers are increasingly turning to experts as the source of trust within each category. Dermatologists in skincare, stylists in haircare and makeup artists in color cosmetics are becoming key validators, raising the bar on performance, proof and authority, and driving premiumization across categories.

Third, there is a heightened expectation for proof of superior, comprehensive performance paired with elevated brand desirability. The brands winning today are those that combine expert-level efficacy with strong emotional and aesthetic resonance.

Against this backdrop, the most compelling areas for investment sit within subcategories where these dynamics are most pronounced.

Dermatological and clinical skincare remains one of the most attractive segments, particularly brands that combine scientific credibility with modern consumer appeal such as Skinfix or Dr. Idriss in the prestige channel. In the professional channel, brands such as Biologique Recherche or Hydrinity could bring deeper professional credibility and access to medspa and in-office distribution.

Longevity-driven beauty, while earlier, represents a strategically important adjacency across both outside-in and inside-out. Brands such as OneSkin on the topical side and Timeline on the ingestible side extend Unilever more meaningfully into true beauty and well-being. Next-generation brands like IM8 further illustrate where the category is heading, as consumers increasingly embrace supplementation as part of a broader longevity-driven beauty routine.

Color cosmetics is one of Unilever’s more notable gaps today. While Hourglass Cosmetics is a strong asset with significant runway, the portfolio would benefit from deeper makeup artistry credentials. Makeup artistry brands with strong professional credibility and cultural relevance such as Patrick Ta Beauty would address this directly while aligning with the broader shift toward expert-led trust.

In haircare, Unilever’s portfolio remains predominantly weighted toward mass, which is a strength from a scale and accessibility standpoint, but leaves meaningful room for premiumization. The next wave of growth is clearly shifting toward professional, scalp-focused, and treatment-led brands, where consumers are increasingly seeking the same level of efficacy, ingredient focus and expert validation they expect in skincare.

Brands like Act+Acre bring expert-led credibility and a treatment-driven approach aligned with this shift. At the higher end, Crown Affair stands out with its positioning around ritual-driven performance, combining efficacy with a differentiated, sophisticated brand experience.

At the same time, brands like Odele Beauty demonstrate how the masstige segment can be elevated through performance and clean, lifestyle-led positioning. This creates a natural pathway for Unilever to continue strengthening its core in masstige while progressively moving upmarket into prestige.

Finally, body care is being rapidly premiumized and sits at the intersection of skincare, wellness, and fragrance. Brands like Nécessaire and Salt & Stone reflect the direction of travel in this category.

Across all of these areas, the common thread is consistent: expert-led credibility, higher proof of performance, and premiumization, delivered through brands with strong desirability and the ability to scale across modern distribution channels.

A more focused, beauty-led Unilever is likely to intensify competition for scaled, high-quality indie assets and raise the bar for what constitutes an attractive acquisition target, with greater emphasis on authority, differentiation and multi-channel strength.

- Adam Louras Partner, Mercenary

The lines separating healthcare services, medicine and beauty and wellness brands have never been thinner, thanks to public telehealth platforms like Hims & Hers, LifeMD and even the newly transformed Weight Watchers (ironically, formerly owned by Unilever). I believe that these all-encompassing, solution-oriented platforms are the future of selling wellness and beauty products.

Consumers are craving convenience, custom curation and privacy more than ever, and these services provide a one-stop shop for solutions to some of the more socially delicate challenges at the intersection of health and wellness: baldness, low testosterone, erectile dysfunction, weight loss, gut health and more.

If I were leading M&A for Unilever, the path forward would be simple: acquire and aggregate the telehealth platforms and gain a monopoly on your products as solutions to envelop each "patient" directly.

Unilever can cross-promote and sell its existing product portfolio to consumers with diverse needs on the back of some of the more medical products and services. For example, Unilever is uniquely positioned to complement the sale of its own compounded GLP-1 products with nutritional supplements that help stave off side effects such as bone loss, malnutrition, and gastrointestinal issues.

Who wouldn't pay up for a curated supplement and topical regimen to help you look and feel your best when you are already shelling out $2,500-plus per month for weight-loss injections? While you're at it, why not grab your Nutrafol hair growth supplements, Olly multivitamins, and your Grüns greens all at once and have them delivered right to your door along with everything else?

- Scott Norton Consumer Venture Investor and Founder, Sir Kensington’s

After selling the spreads and tea businesses, spinning off the ice cream business as a listed company, and now merging its foods business into McCormick, Unilever has migrated into a leaner company with higher margin, e-commerce-friendly products focused on personal care, beauty and wellness. Geographically, it’s been disproportionately active in the U.S. for new acquisitions, putting this country in the spotlight for its future growth and M&A strategy.

Setting the stage, the so-called K-shaped dynamics in the U.S. have given rise to a new class of what I call “superconsumers,” with the top 10% households by earnings in America responsible for 50% of consumption, according to the WSJ. This has made the U.S. the unquestionable center for premium CPG innovation.

Beyond traditional premiumization, however, these superconsumers have favored products that blur the line between beauty and wellness, appealing to both vanity and virtue. For instance, cosmetics products increasingly include skincare actives, and nutrition products like Grüns present as a bag of candy.

If I were Unilever, I’d continue hunting for brands with mainstream appeal that combine beauty and wellness. Nutrafol is a prime example of this, being a novel supplement with a distinct brand, positioned as a hair health product with a chiefly cosmetic result.

Another growing trend that could influence M&A is the quantification of self-measurement that comes from Oura rings, Apple watches and the many biomarker diagnostic companies. With the influx of data and newly known deficiencies consumers are learning about, there will be opportunities to tie into these services and deliver solutions. If a supplement brand can successfully be seen as part of this feedback loop, that could be highly attractive.

Finally, I would look for M&A targets that offer complementary and transformational capabilities, not just a beloved brand. A decade ago, a story was told about DTC capabilities getting absorbed into parent companies from digital-native acquisitions, but that turned out to be difficult in practice. When it comes to AI capabilities, it’s got the potential to be different.

I’ve talked to a few CPG startup founders who are elite users of AI, building analytics, marketing and product development engines with minimal coding skills that would have been impossible a year ago. With the sheer amount of data and broad portfolios Unilever has, the right AI evangelist brands acquired into the company could be applied to their $46 billion business.

- Tyler Morgan Principal, BFG Partners

From my perspective, Unilever should prioritize high-frequency, consumable wellness categories with strong repeat and pricing power, things like supplements, functional personal care and condition-specific solutions. Adjacency gaps like color cosmetics seem more fleeting and less durable from a revenue perspective.

Unilever has two of the most successful consumer acquisitions of the last decade in Nutrafol and Liquid I.V. The focus should be on brands with demonstrated retention, multi-channel durability (DTC + retail) and a margin structure that improves at scale. I think that is represented in the Grüns acquisition as well.

- Odile Roujol Founding Partner, Fab Co-Creation Studio Ventures

The market has so many offerings. It’s the Wild West. Outside of exceptional metrics (Grüns), I would now focus on premium supplements and beauty ingestible brands with clinical tests on human beings and experts (doctors, dermatologists) prescribing them. I would look for brands demonstrating multi-year growth with loyal customers and a subscription model.

Unilever is already thinking along these lines. It’s interesting to see it has invested in Novos, which focuses on longevity supplements and epigenetic tests measuring biological aging.

If you have a question you'd like Beauty Independent to ask investors, consultants and marketers, send it to [email protected].