The goalposts for securing beauty funding have never been higher, but the field of play is more open than ever, at least according to XRC Ventures’ latest quarterly Consumer VC Benchmarks report based on a survey of 16 European and American beauty investors.

Investor appetite for beauty hasn’t diminished. Conducted in April and May, the survey, which included investors from firms such as Sugar Capital, Selva Ventures, Springdale Ventures, BAM Ventures, Fab Co-Creation Studio Ventures, True Beauty Ventures, Palette Ventures and Five Seasons Ventures, found that 56% of respondents plan to deploy more capital in beauty and personal care this year, while the rest expect to maintain their investment levels from last year.

As beauty and wellness continue to converge, investors are looking beyond traditional beauty categories. Oral care is attracting greater attention, joining haircare, scalp care, body care and fragrance among the categories drawing the strongest investor interest. Fragrance emerged as a standout in the report, with investors singling out its premium pricing power and expansion opportunities. Sexual wellness, men’s grooming and color cosmetics were named the least attractive categories.

“We remain highly constructive on the broader beauty landscape, with particular conviction in science-based haircare,” says Rana Taghdisi Argenio, founding partner at Palette. “Demand is being driven by a confluence of factors, including an aging population, increased incidence of hair loss among menopausal women, the impact of GLP-1 usage and rising stress-related lifestyle effects. Within this context, we are especially focused on brands addressing hair strength and hair loss through efficacious, clinically supported formulations at accessible price points.”

Dedicating time to meeting with oral care brand founders, Lisa Sugar, general partner and co-founder at Sugar Capital, says, “The oral care microbiome is becoming very popular from a health and wellness perspective, and we would love to see updated products and options beyond what is on the shelves already. We need cleaner, better-for-you options, and they are coming.”

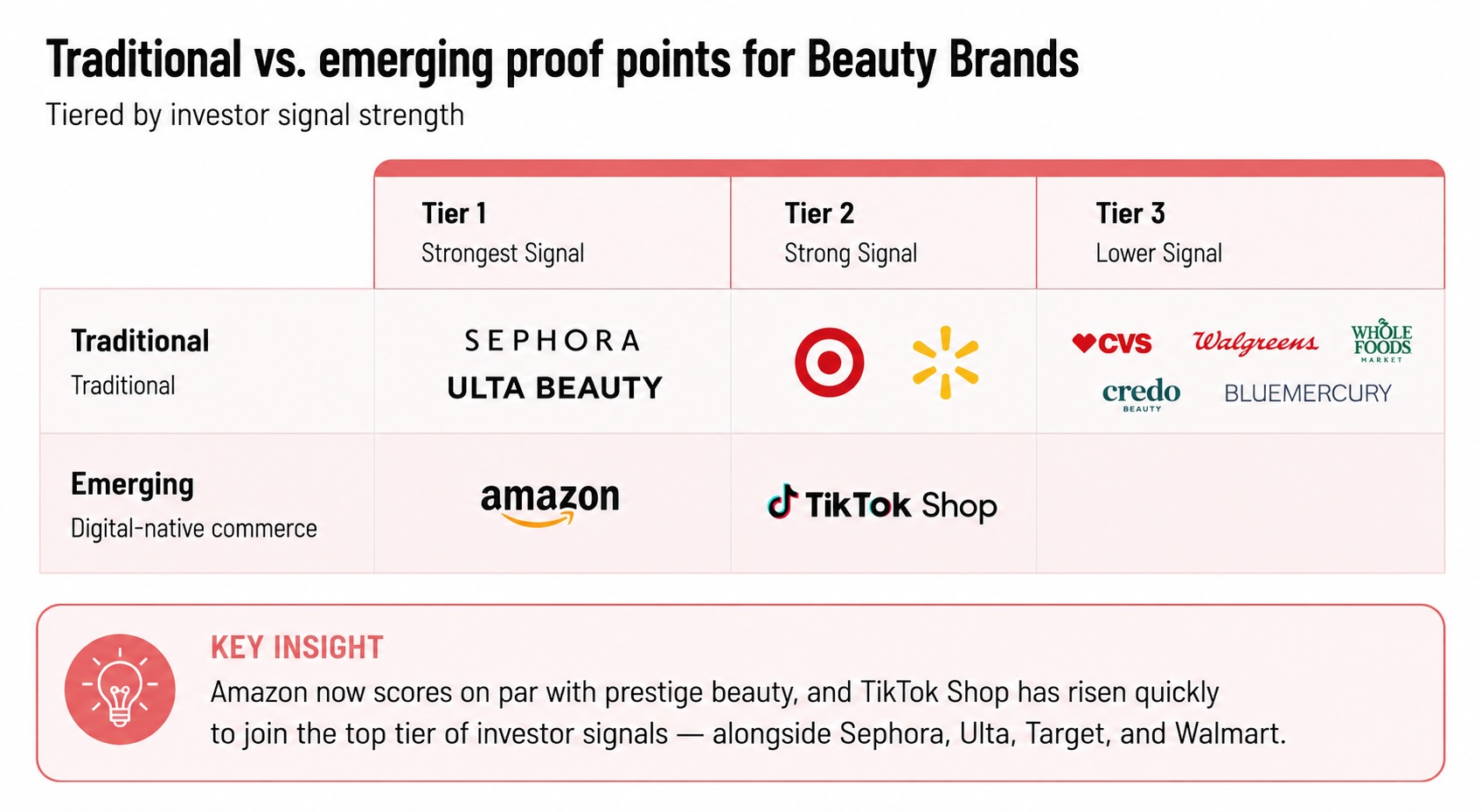

For prestige beauty brands, a Sephora launch has long been considered one of the clearest paths to an eventual strategic exit, with brands such as K18, Briogeo, Living Proof, Drunk Elephant, Ouai and Youth To The People following that trajectory. However, investors are no longer convinced Sephora is the only route to creating value and scale in beauty.

XRC’s survey respondents weighted Amazon as highly as major beauty specialty retailers Sephora and Ulta Beauty. They identified success on TikTok Shop, beauty’s fastest-growing platform, as an auspicious sign of momentum and product-market fit. Grocery, professional beauty channels, drugstores and smaller beauty specialty retailers like Credo and Bluemercury, which the report points out generally don’t drive meaningful revenue, were weighted less favorably.

“I still believe Sephora is best-in-class when it comes to building masstige and prestige beauty brands. That said, the level of investment now required to succeed there has increased dramatically,” says Diana Melencio, general partner at XRC’s Brand Capital Fund. “As a result, alternative channels are becoming increasingly attractive entry points, and for challenger brands, it may make sense to wait longer before entering Sephora given the associated capital burden.”

She adds, “At the same time, Target, Ulta Beauty and Walmart are making meaningful investments in beauty and wellness in-store, creating more viable paths to brand building and ‘kingmaking’ capabilities. In my view, the biggest challenger is Amazon, which is both the default destination for replenishment and the primary beneficiaries of product discovery on TikTok, e.g. K-Beauty 2.0.”

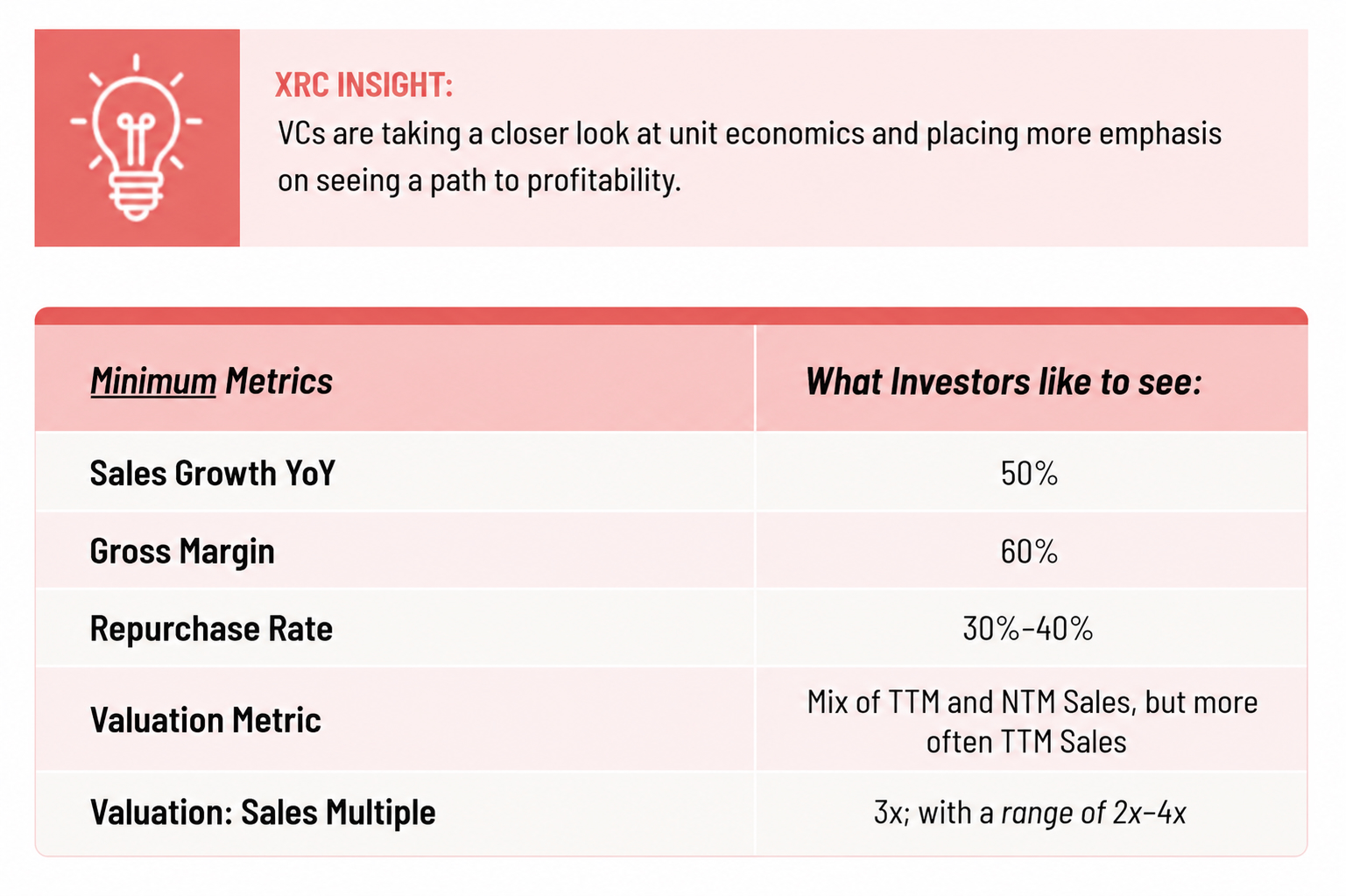

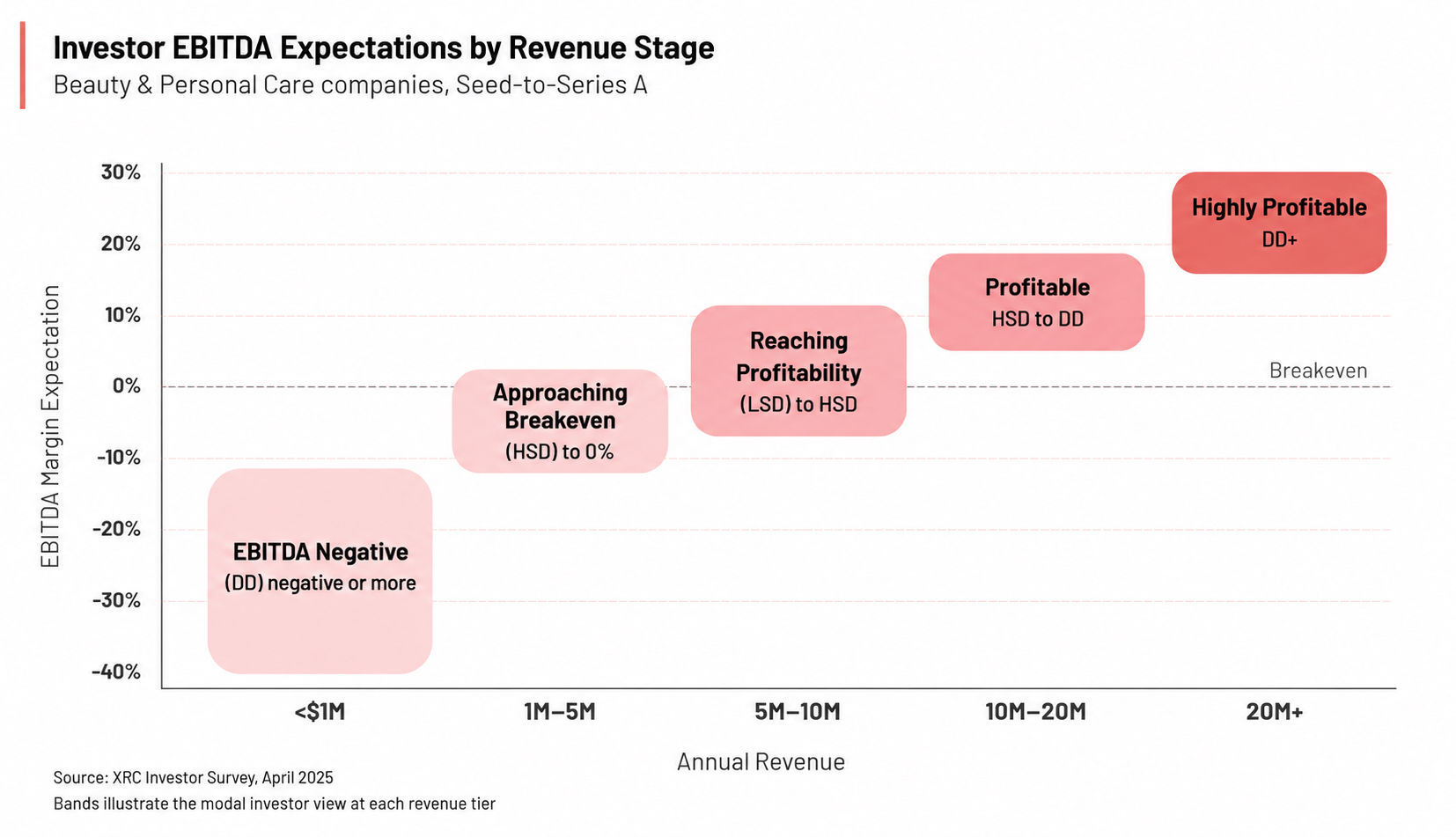

Investors told XRC they are prioritizing sales growth and repurchase rates, with profitability expected once brands reach $5 million to $10 million in sales and double-digit earnings before interest, taxes, depreciation and amortization (EBITDA) margins expected when companies hit $20 million in revenue. For early-stage brands, investors generally want to see 50% year-over-year sales growth, gross margins of at least 60% and repurchase rates of 30% to 40%.

The fragrance category embodies the characteristics beauty investors are seeking, especially as younger consumers embrace it and shoppers are willing to pay more for it. XRC highlights that fragrance-centered brands such as Homecourt, Touchland and Salt & Stone can price products 3X to 6X above entrenched category leaders.

Gen Z consumers turn to fragrance as a form of self-expression. They’re adopting fragrance wardrobing or assembling a collection of fragrances—they’re estimated to own as many as eight to 12 fragrances versus two to three for boomers—and fragrance stacking or layering multiple scented products, from conventional fragrance formats to laundry detergent and deodorant. XRC underscores that these dynamics are leading to higher lifetime values for fragrance brands, expanded distribution, deeper loyalty, earned media and stronger margins.

“Young customers layer scents and make their signature personalized and according to their mood of day,” explains Odile Roujol, founder of Fab Co-Creation Studio Ventures, in XRC’s report. “It’s a totally different story versus the past behaviors of gen X and even millennials.”

As they hunt for fragrances, gen Z consumers are scouring TikTok, with 66% of them saying TikTok influences their fragrance purchases, according to market research firm Circana, and #FragranceTok surpassing 39 billion views, according to consumer insights firm Spate. Still, Circana approximates that brick-and-mortar accounts for about 75% of fragrance sales in the United States, the highest share of any beauty category.

These shifting consumer behaviors are opening the door to disruption by indie brands. Indie brands account for 29% of the U.S. fragrance market, below the 32% share they command in beauty overall, but they’re growing 46% year over year, the fastest rate for indie brands by beauty category. Fragrance launches rose 50% in 2025, according to Circana, underscoring the rush of newness into the category.

XRC notes that deals involving fragrance and fragrance-adjacent brands have largely achieved sales multiples of 3X to 7X revenue. The firm spotlights several categories connected to fragrance as promising, including home fragrance, with brands such as Laundry Sauce, DedCool, Guests on Earth and Homecourt; functional and wellness-oriented fragrance, with brands such as The Nue Co., Gymspin and MNML; personal care, with brands such as Corpus and Salt & Stone; clean fragrance, with companies such as Henry Rose, Lucent and Layermor; and fragrance dupes, with brands such as Dossier, Fine’ry and Mozi Wash.

In the report, Valerie Evans, principal at Five Seasons Ventures, says, “Fragrance is permeating every area of beauty, from haircare to body care and beyond. We’re particularly interested in the intersection of fragrance and functionality such as modernized aromatherapy and functional haircare (that does not smell functional.)”

Fragrance has hot spots across the mass and prestige segments. In the first quarter this year, U.S. fragrance sales were up 7% in prestige, which accounts for two-thirds of the category, and 16% in mass, according to Circana. During a panel at Beauty Independent’s Dealmaker Summit earlier this month in New York, Melencio, Cassandra Grey, founder of Violet Grey; Umberto Doni, CEO and co-founder of Giardini di Toscana; and Shaun Westfall, managing director for lifestyle, wellness and beauty investment at investment bank North Point, discussed those hot spots.

Westfall called out Dossier’s winning formula in mass as an example of how brands can gain traction through innovation, social media, retail partnerships and accessible value propositions. Westfall’s firm, North Point, served as exclusive financial advisor to private equity firm American Pacific Group on its investment in Dossier announced in April.

Comparing the brand to E.l.f. Beauty, Westfall said, “There’s a whole bunch of consumers that just can’t afford a $200 fragrance, but they can afford $50 or buy three or four $50 fragrances, and they can layer a wardrobe like the aspirational girl down the street.”

If Dossier illustrates the potential of accessible fragrance, celebrity and influencer brands such as Orebella, whose series A round led by Silas Capital was disclosed last month, demonstrate how fragrance can serve as a cultural and lifestyle purchase. Referring to Bella Hadid’s brand, Westfall argued consumers buy into the person and world surrounding a fragrance, not simply the scent itself.

“I’m buying a price of admission into her life,” he said. “I can’t live her life, but if I wear her fragrance, I can sort of be a part of it.”

Click here to secure Early Bird tickets to Dealmaker Summit running Nov. 9 to 10 in London.

Leave a Reply

You must be logged in to post a comment.